The Quiet Reorg: AI is Redrawing Financial Services Org Charts

Nobody got a layoff notice. The reorg is happening at the hiring gate.

Hiring of workers aged 22-25 in AI-exposed occupations is down 14% since ChatGPT launched.

No press releases.

No severance packages.

No angry threads on LinkedIn.

The entry-level pipeline is quietly narrowing, and four major research reports published in recent months converge on the same conclusion: firms that treated AI as a technology purchase instead of a people investment have hollowed out their talent pipeline without building anything to replace it.

I’ve been reading these reports as they dropped — Anthropic, McKinsey, the NBER, Deloitte.

Read together, they describe a fundamental mismatch that most financial services leaders haven’t named yet.

Naming it is the first step to fixing it.

The four reports at a glance:

Anthropic — “The Economic Impacts Study” (March 5, 2026)

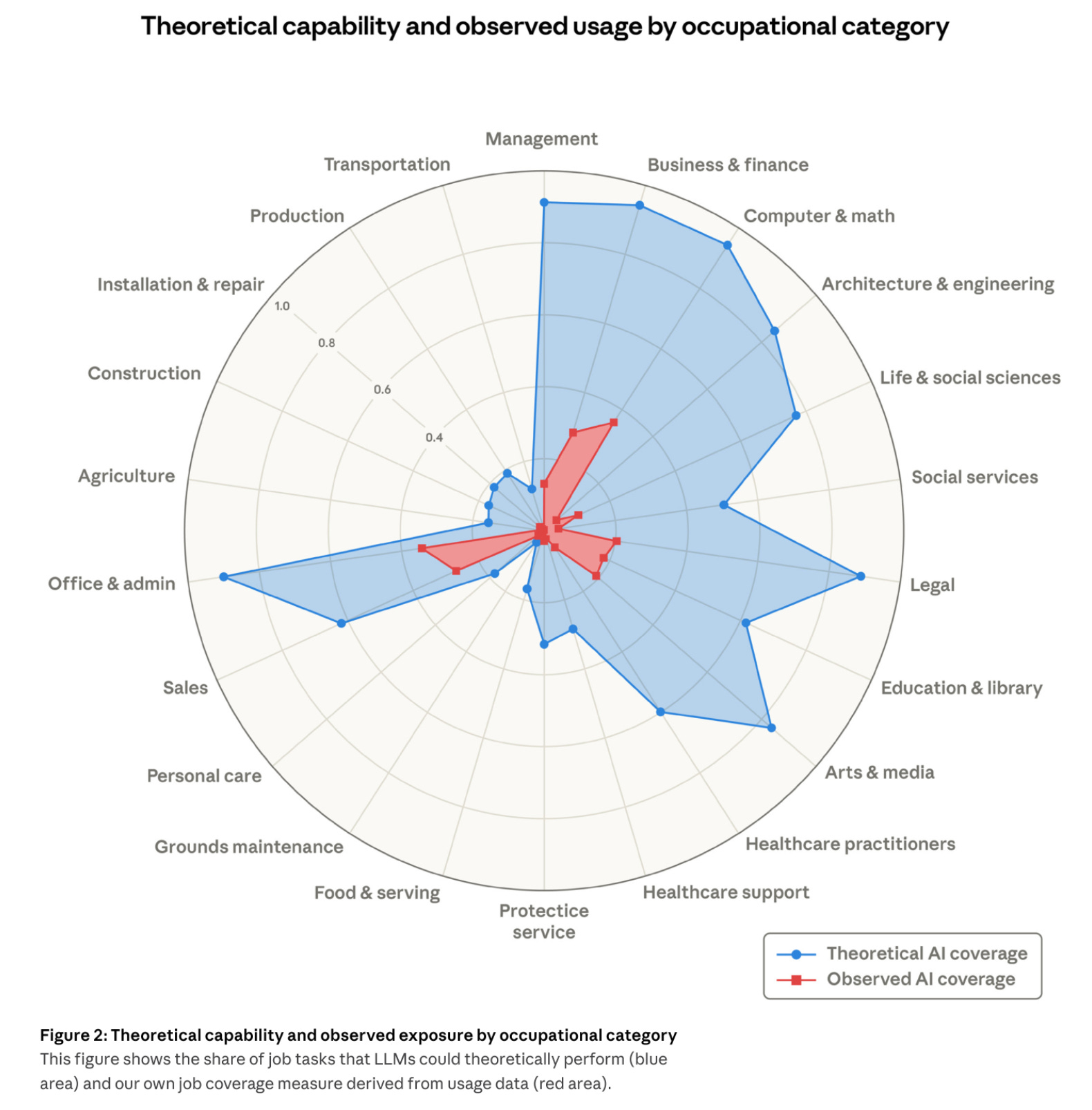

Mapped AI’s theoretical capability against observed real-world exposure across occupations and industries.

Used labor market data to track what’s actually changing in hiring, wages, and employment patterns post-ChatGPT.

The first empirical displacement study from a frontier model lab.McKinsey — “The State of Organizations 2026”

Surveyed 10,018 leaders across industries and geographies on organizational health, AI readiness, and the barriers to capturing value.

Includes detailed case studies (Allianz, a P&C insurer)

The $1-to-$5 investment ratio that anchors much of this analysis.NBER — “AI Adoption, Employment and Productivity” (2026)

Firm-level survey of ~6,000 companies across the US, UK, Germany, and Canada.

Tracks actual AI adoption rates, productivity effects, and employment predictions by sector.

Finance and insurance emerges as the highest-adoption sector in the UK.Deloitte — “TMT Predictions 2026” (November 2025)

Annual technology forecast covering agentic AI, SaaS disruption, and digital labor integration.

Projects the AI agent market from $9B to $35-45B by 2030.

Maps three deployment approaches firms are taking.

The displacement nobody announces

Anthropic’s Economic Impacts Study, published March 5th, mapped theoretical AI exposure against what’s actually happening in the workforce. The headline finding isn’t mass unemployment.

Financial and investment analysts rank as the 7th most exposed occupation, with 57.2% observed exposure. Computer programmers sit at 74.5%. Customer service representatives at 70.1%.

No systematic unemployment increases in these roles.

The displacement is subtler.

Companies aren’t firing analysts. They’re not replacing the ones who leave, and they’re not hiring the next cohort at the same rate. The org chart shrinks from the bottom, one unfilled requisition at a time.

Meanwhile, the people still inside the building are already using AI without telling anyone. That gap between official adoption and actual usage makes the compression invisible from the top.

This isn’t a blue-collar story. Graduate degree holders are 3.9 times more exposed to AI than those with only a high school education. Workers in exposed occupations earn 47% more on average ($32.69/hr vs. $22.23/hr). AI is compressing the knowledge-worker tier, the very roles financial services firms built their operating models around.

The young workers who do get in are adapting faster than their managers expect, which only widens the gap between how firms plan and how work actually happens.

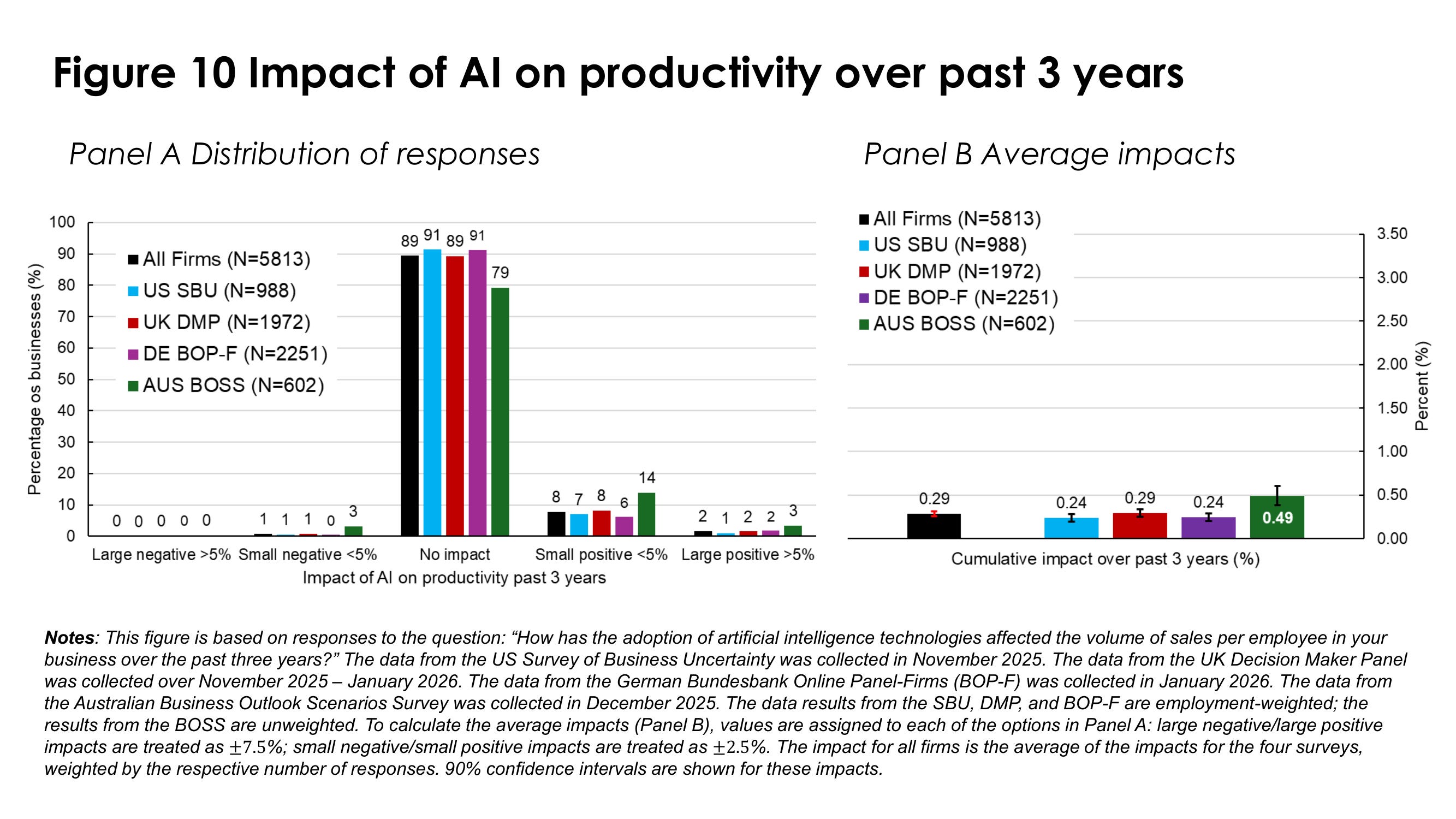

The NBER’s firm-level data tells the same story from the employer side. Between 89% and 95% of AI-using firms report “no impact” on current employment over the past three years. Those same firms predict +1.4% productivity gains alongside -0.7% employment effects over the next three. US firms specifically expect -1.19% employment reduction. UK firms, -1.36%.

That’s not a wave of layoffs.

It’s a slow tide going out…

Each number is small enough to ignore in any given quarter. Compounded across a sector over three years, it reshapes who works where.

UK AI non-use dropped from 45% to 25% in ten months. Finance and insurance leads UK adoption. The acceleration curve is steep, and hiring compression will follow.

Firms getting AI right are also paying more. NBER found that AI-adopting firms correlate with higher labor productivity and higher wages per employee.

They aren’t cutting costs on people.

They’re concentrating investment in fewer, higher-skilled roles.

Whether anyone is building the pipeline to fill those roles in five years is a different question.

The $5 problem nobody’s funding

McKinsey surveyed over 10,000 leaders globally for their State of Organizations 2026 report. The number that should bother financial services executives:

86% feel unprepared for AI in daily operations.

Only 6% are realizing AI’s full value.

Less than 20% see meaningful bottom-line impact.

The core finding is blunt:

for every $1 spent on AI technology, organizations need $5 on people readiness — reskilling, change management, workflow redesign.

Most firms have the ratio inverted. They bought the tools. They skipped making their people capable of using them.

I wrote about this exact failure mode a month ago: the bottleneck was never the technology. It was always the skills gap.

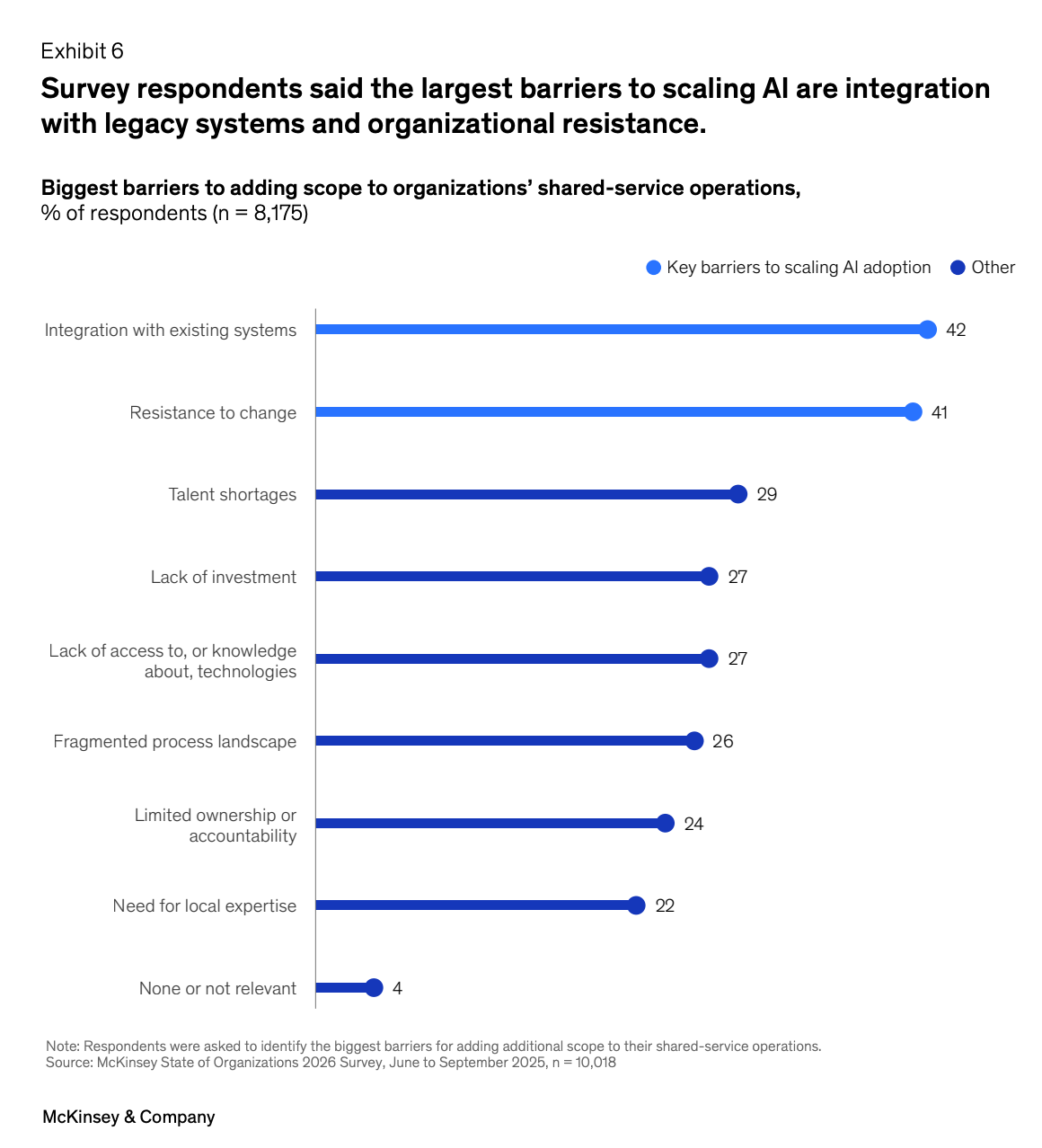

The top three barriers are all human problems:

concerns about AI (46%),

regulatory and ethical worries (44%),

organizational change management (39%).

The top three enablers mirror this:

ease of use (42%),

leadership championing (36%),

a dedicated team (36%).

One in six organizations has no C-level owner for AI adoption. Not a distributed ownership model.

No owner at all. In 1 in 6 companies!

Even where ownership exists, the strategy evaporates before it reaches execution.

40% of C-suite leaders say they understand their AI strategy.

Only 27% of middle managers agree.

That 13 percent gap means the strategy isn’t surviving the organizational resistance. It’s a slide deck in a Teams’ site.

There’s a resource problem stacked on top. 41% of leaders cite resource reallocation as a barrier. They know where the money should go. They can’t move it.

Budgets are locked into structures, teams, and vendor contracts built for a different era.

One firm McKinsey profiled audited itself:

60% excess meetings,

35% duplicate decisions,

two-month data lags,

1,000+ hours per month of manual reporting.

AI can’t fix that.

You fix the organization first, then deploy AI into workflows that actually work.

Automating a broken process just produces broken outputs faster.

What Allianz figured out

Allianz CHRO Bettina Dietsche: “In five years, two-thirds of the skills we need will be completely different.” They didn’t treat that as a theoretical concern.

They built AllianzGPT and got 60,000+ active users.

They integrated AI into underwriting, claims processing, and product design. Their employees average 43+ hours of learning per year, and employees voluntarily pushed it to 60. A P&C insurer in the same McKinsey research achieved 95% user acceptance on AI-assisted claims review.

The difference between Allianz and the 86% who feel unprepared isn’t the technology.

Allianz didn’t buy a better model.

They invested in making their people capable of working alongside it, then measured acceptance rather than just accuracy.

McKinsey’s data: firms that invest in people alongside technology are 4.3x more likely to stay in the top quartile.

NBER backs this from a different angle — wage growth is the strongest predictor of AI productivity gains. Firms paying more per employee get more AI value.

The people investment shows up directly in the numbers.

Firms that invested early in people readiness attract better talent, get more from their AI deployments, and build institutional muscle that grows over time.

Firms that bought tools without investing in people are stuck in a loop:

tools underperform,

which makes the case for people investment harder,

which means the tools keep underperforming.

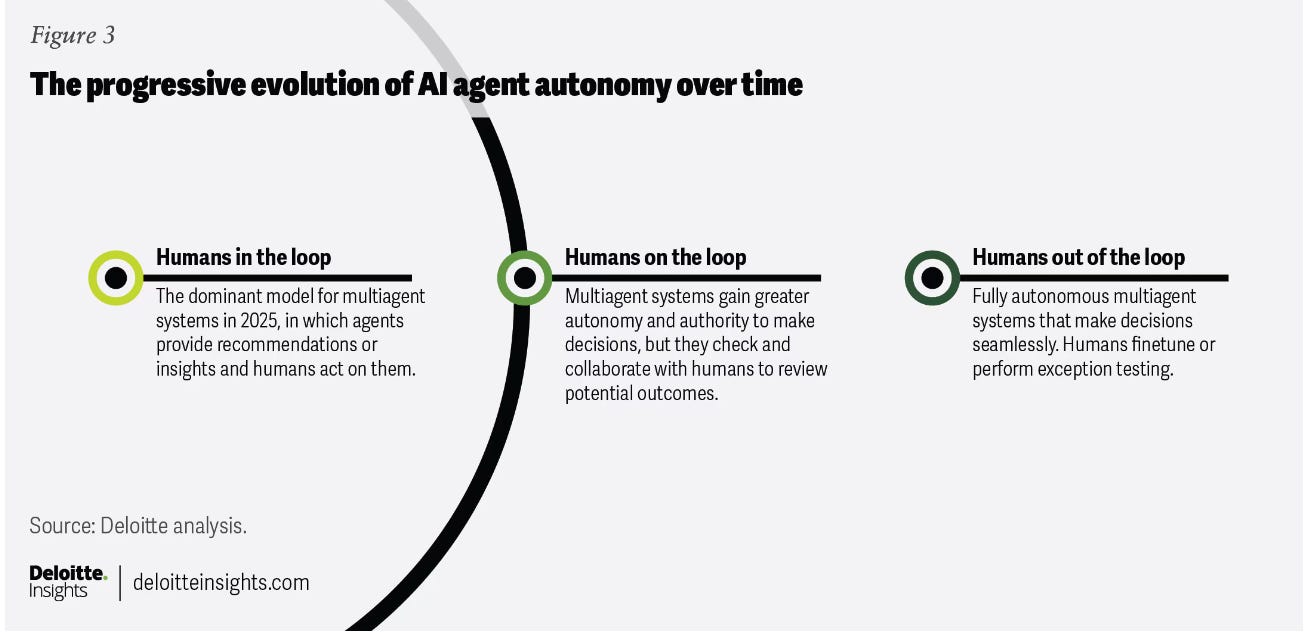

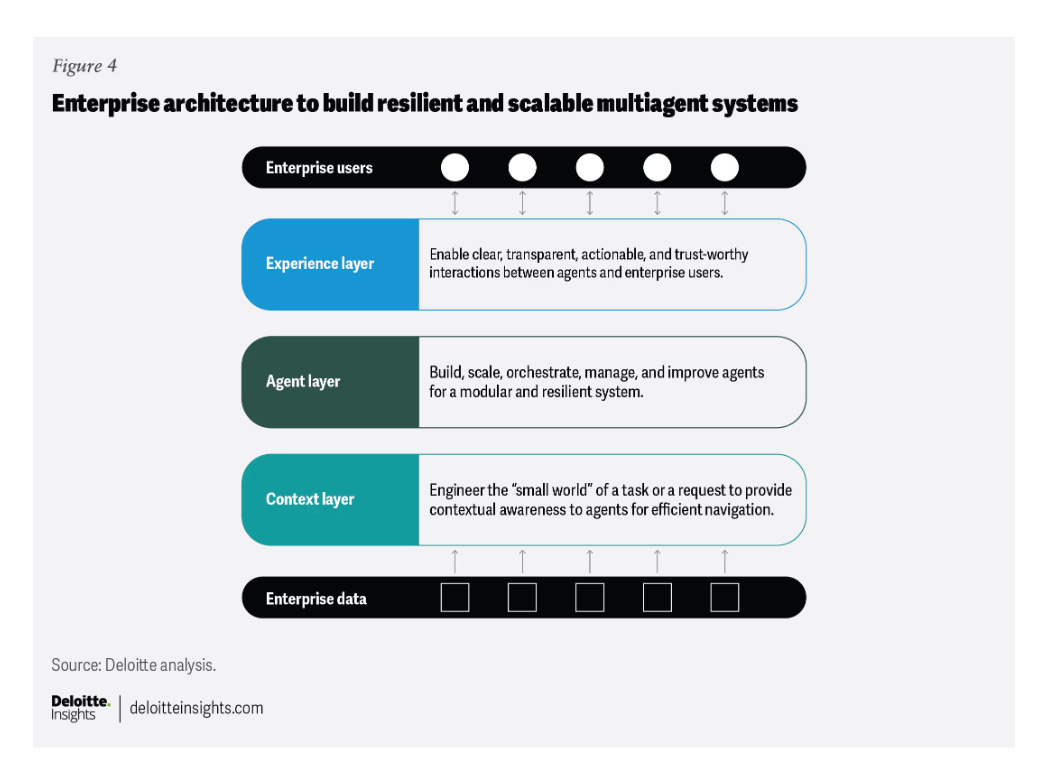

The agent layer compresses the timeline

Everything above is the current state.

Deloitte’s TMT Predictions 2026 describes what’s next.

The AI agent market is projected at $9 billion in 2026, growing to $35-45 billion by 2030.

Agent orchestration is already deployed in financial investment research. By 2028, 33% of enterprise software is expected to include agentic AI capabilities.

Only 28% of firms believe they have mature agent capabilities, versus 80% who feel confident about basic automation. That 52-point gap matters. 86% of CHROs see digital labor integration as a central strategic priority, yet 40% of agentic AI projects could be canceled by 2027.

The business model is shifting underneath firms still negotiating seat licenses.

40% of enterprise SaaS is expected to move to usage or outcome-based pricing by 2030. (I intend to write more on the SaaS pricing strategies soon - it’s afascinating landscape!)

35% of current SaaS functionality could be replaced by AI agents.

83% of AI-native SaaS companies already price this way.

I wrote about the SaaS pricing model collapse two weeks ago — the agent layer is the mechanism driving it.

Deloitte identifies three approaches to agent deployment:

smart overlay on existing systems,

agentic by design for new builds, and

full process redesign.

The companies that only add AI on top of old systems are the same ones McKinsey identified as failing to invest enough in training their people.

For financial services, agents doing investment research, claims triage, compliance monitoring, and customer service create a category of “digital labor” that doesn’t fit existing workforce planning models.

The CHROs see it coming.

The operational capability isn’t there yet.

What to do about it

Four reports. Same finding. The companies winning at AI are investing in their people first.

The firms lagging behind are investing in tools first.

The agent layer is about to widen that gap.

Actions, by urgency:

This month:

Audit your AI investment ratio against the $1:$5 benchmark. For every dollar going to AI technology, how much goes to reskilling, change management, and workflow redesign?

If you can’t answer that from your current budget data, that’s the first problem.Check whether you have a named executive owner for AI adoption. Not a committee. A person. NBER found that in the UK, CFOs lead AI adoption over CEOs (50% vs. 34%).

The question is whether the right person owns it — someone who controls budget.

This quarter:

Map your entry-level pipeline exposure. Which roles are you hiring fewer of? Is that intentional, or is it happening by default as managers quietly close requisitions?

Compressing from the bottom without building a development pathway for existing staff creates a skills gap that surfaces in three to five years.Pick one AI-assisted workflow. Deploy it with structured learning support, not just a tool rollout.

Measure user acceptance, not just model accuracy. If acceptance is below 80%, the problem isn’t the AI.

This year:

Assess which workflows are candidates for agentic AI. Map the gap between your basic automation confidence and your agent readiness. If you need a framework for evaluating where your AI capabilities actually stand, the benchmarks guide is a starting point. Then use Deloitte’s three-tier framework: smart overlay, agentic by design, or full process redesign. Most firms default to overlay. The ones getting results are doing redesign.

The 86% who feel unprepared aren’t wrong. They’re running out of time to change it.

The hiring gates are already narrowing.

The agent layer is arriving.

The firms that figured out the people investment three years ago are 4.3x more likely to be outperforming everyone else.

When was the last time you checked whether your firm’s AI investment is going to tools or to the people who need to use them?

What ratio did you find?

References: