The SaaSpocalypse: $285B in smoke, and the question nobody's asking

$285 billion in software valuations vanished in 48 hours. The market thinks AI is coming for SaaS. The market is half right.

On February 3rd, 2026, someone at Jefferies typed “SaaSpocalypse” into a research note, and within hours traders were selling.

Thomson Reuters dropped 16% -- its worst single day ever.

RELX fell 14%.

LegalZoom cratered 20%.

The software sector ETF had already been sliding since September, but this was different.

This was a stampede for the exits.

What triggered the panic wasn’t a single event. It was a pile-up. Anthropic had released a legal plugin for Claude on January 30th -- a 200-line markdown prompt that could triage NDAs, flag non-standard clauses, and generate compliance summaries. (I wrote about Anthropic’s divergent approach to AI automation before the selloff -- the legal plugin was the logical next step.)

A week later, a startup called Base44 announced it had canceled $350,000 a year in Salesforce licenses after vibe-coding a replacement. Matt Shumer published “Something Big Is Happening” and it racked up tens of millions of views.

The narrative locked into place: AI is eating software. Sell everything.

And honestly? The bearish case writes itself.

The fear is not irrational

Look at the numbers.

Microsoft is sitting in a 26% drawdown.

Oracle has been cut in half.

The IGV software ETF plunged 28% from its September 2025 peak.

KPMG, yes KPMG, used AI as a negotiation weapon to squeeze its auditor Grant Thornton on fees, pushing them from $416,000 down to $357,000. That’s a 14% haircut, and the explicit reasoning was: AI makes this work cheaper now. Pass it on.

Cursor AI is achieving over 1,000 code commits per hour. Autonomous coding agents producing working software at a pace no human team can match. That’s a different category of threat than anything we’ve seen from developer tooling.

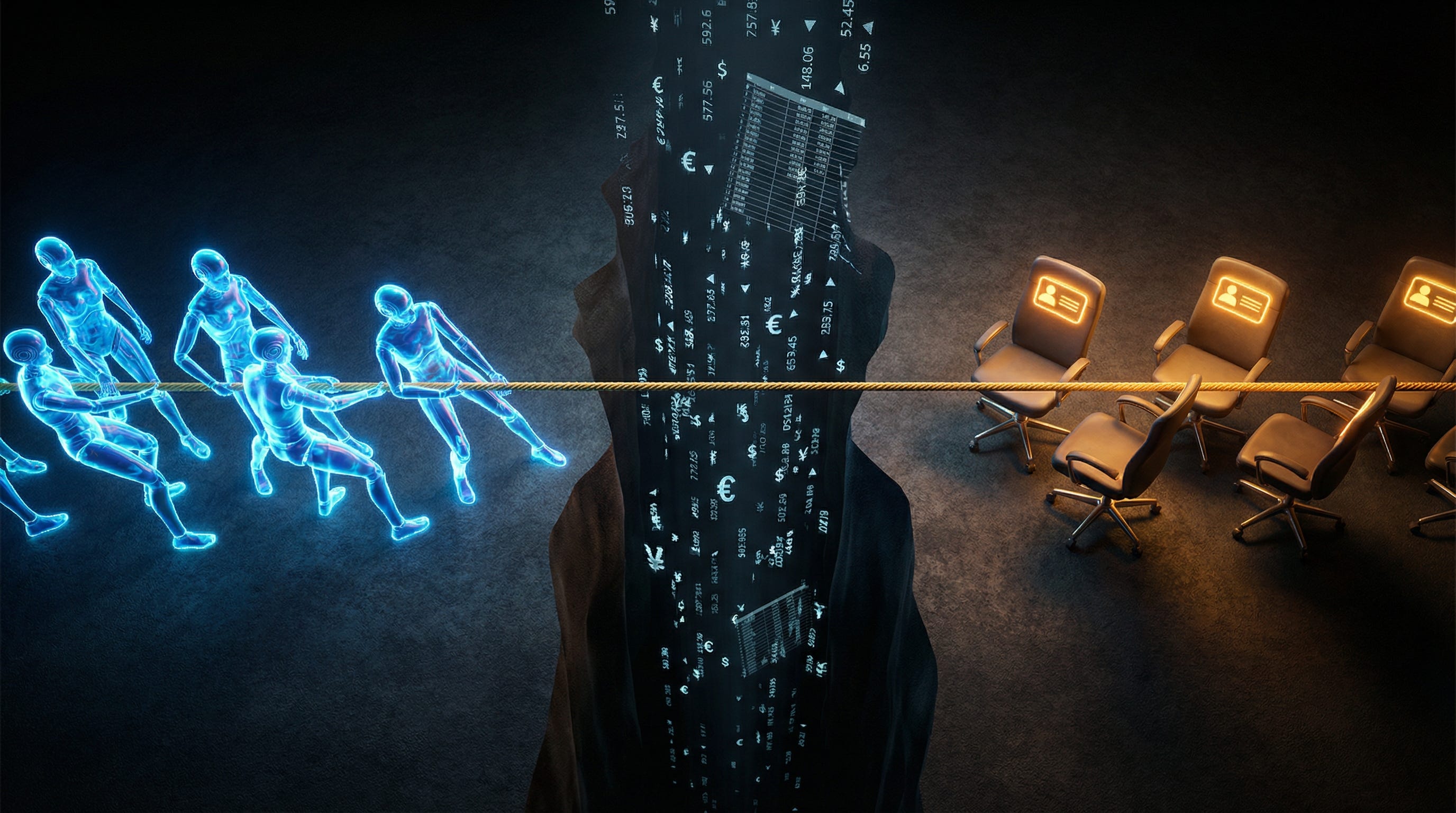

The fear driving the selloff is straightforward: if AI agents can do the work, why are we paying per-seat licenses for humans to log in and click buttons?

Satya Nadella himself trolled Salesforce at a conference, saying SaaS would “dissolve into agents sitting atop CRUD databases.” When the CEO of the world’s largest software company tells you the category is dissolving, people listen.

And the vibe-coding movement isn’t theoretical anymore. Founders are genuinely canceling enterprise contracts and rebuilding tools with AI in weeks.

The old SaaS sales pitch “it would take you 18 months and $2 million to build this yourself” sounds increasingly hollow when a capable developer with Claude or Cursor can prototype a replacement over a long weekend.

But here’s what the panic sellers are missing

Finbarr Taylor made a point the market hasn’t absorbed yet: you can clone the interface, but the interface was never the product.

A SaaS platform is the ten years of edge cases baked into it. The compliance certifications. The audit trail. The integrations with 200 other systems that all need transactional consistency.

Anyone who’s tried to rip out a deeply embedded enterprise tool knows the real cost isn’t the license, it’s the migration risk, the regulatory exposure, the thing you didn’t know the old system was doing until it stops doing it.

Bank of America analyst Vivek Arya pointed out something the market seems allergic to acknowledging: investors are simultaneously pricing in two mutually exclusive scenarios.

Either AI capex is deteriorating (bad for the hyperscalers building it),

or AI is destroying SaaS (which requires massive AI capex to happen).

Both stories can’t be true at the same time. Panic doesn’t do nuance.

(If you want to understand the physical infrastructure underpinning this capex, The Chip War is essential reading.)

There’s also what’s now being termed the Articulation Bottleneck.

A human’s vague intent “I need a CRM” represents less than 1% of the information needed to build a useful tool. The other 99% is workflow logic, permission hierarchies, data validation rules, compliance requirements, and integration specifications that nobody writes down because they’re embedded in institutional knowledge.

Vibe-coding a replacement for a weekend project is one thing. Vibe-coding a replacement for a system that processes $400 million in quarterly transactions is a different conversation entirely.

Michael Pollan once argued that “nutritionism” - reducing food to its individual nutrients - misses the point of eating.

Something similar is happening here.

Reducing SaaS to its lines of code misses the point of enterprise software. The code is the least interesting part.

Both arguments have a blind spot

Something structural is breaking. Enterprise software isn’t going anywhere. What’s actually dying is the per-seat pricing model, and both sides of the debate keep talking past it.

When AI agents do the work, they don’t log in. They don’t need a seat. They don’t show up in your active user count.

The entire economic architecture of SaaS is to charge per human, per month, scale with headcount and this collapses when the work shifts to agents that operate through APIs.

This is why Thomson Reuters got destroyed while the underlying demand for legal research didn’t change. Nobody stopped needing to review contracts.

The market just realized that charging lawyers $200 per seat per month is indefensible when a 200-line prompt does the triage work.

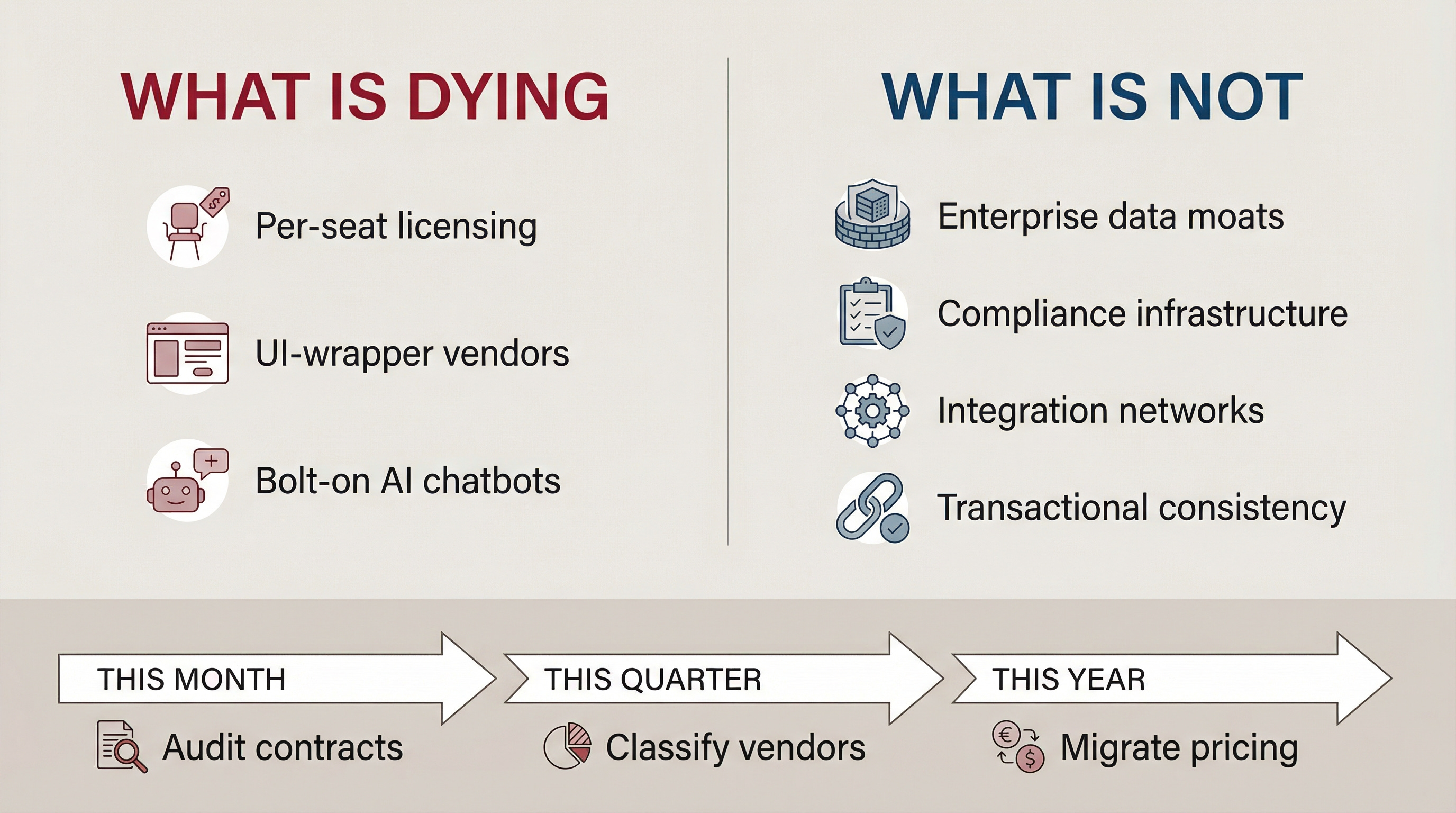

The vendors that will survive are the ones rebuilding for agentic-first architecture pricing on outcomes, on transactions, on value delivered. Everyone else is bolting a chatbot onto a legacy UI and calling it an “AI feature.”

That’s putting a touchscreen on a typewriter.

Nadella’s trolling of Salesforce was funny, but here’s the irony: the same logic threatens Microsoft Office.

If agents are sitting atop CRUD databases, why does anyone need Excel? The disruption doesn’t care about your market cap.

What this means for leaders

Every enterprise technology leader needs to audit their SaaS portfolio against a simple question:

Are we paying for access to a platform, or are we paying for access to a user interface?

If the answer is “user interface,” that contract is on borrowed time. If the answer is “platform” then the data, the workflows, the compliance infrastructure, the integration fabric and that vendor still has a place in the future of an enterprise.

A different-shaped and priced moat than it had two years ago, but still a moat.

This month:

Pull your top 10 SaaS contracts by spend. For each one, ask: what percentage of the value is the UI vs. the underlying data and workflow engine? If you can’t answer that question, you don’t understand your own stack well enough. (My guide to cutting through AI vendor benchmarks applies here too -- the same skepticism you need for model evals, you need for SaaS vendor claims about their “AI features.”)

Identify which vendors are pricing per-seat vs. per-outcome. The ones still clinging to seat-based models are telling you something about how seriously they’re taking the shift.

This quarter:

Run a small experiment. Pick one internal tool that’s pure UI -- something your team uses for data entry or simple lookups -- and see what it takes to replace it with an agentic workflow. Not to save money. To learn where the actual complexity hides. It hides somewhere you don’t expect.

Renegotiate at least one contract using the KPMG playbook. If AI is making the work cheaper, the savings should flow to you, not just to your vendor’s margin.

The companies that figure out what they’re actually selling whether its data, workflows, trust, compliance, will reprice and survive.

The ones that were really just selling a nice interface are in trouble. IMHO.

What’s the first SaaS contract in your portfolio that fails the “platform vs. UI” test?

References: