Per-Seat Pricing Is Dying. Your SaaS Contract Shouldn't Go With It.

Jefferies slashed Workday’s price target by 54%. Then Workday beat earnings. Someone is wrong — and enterprise operators know who.

On February 23rd, Jefferies analyst Brent Thill cut Workday’s price target from $325 to $150. DocuSign from $105 to $45. The thesis: AI is eating enterprise software alive. Three days later, Workday reported Q4, beat estimates ($2.47 vs. $2.32), and grew its contracted forward revenue 15.8%. The stock still fell 10%.

That gap between what the market is pricing and what the balance sheet shows? That’s the signal.

Post #11 diagnosed the $285B selloff and asked: is this the death of software, or the death of a pricing model?

What does an enterprise leader actually do with this moment?

The broken logic

JP Morgan nailed the contradiction in a single phrase: “broken logic.” The market is simultaneously pricing in two beliefs

AI will destroy SaaS revenue streams

AI infrastructure spending is overvalued.

Both can’t be true.

If AI agents are replacing enterprise software at scale, the companies building those agents should be worth more, not less. If AI infrastructure spending is a bubble, the SaaS replacement thesis collapses with it.

Gartner forecasts enterprise software spending will grow 14.7% in 2026 to $1.4 trillion. Not shrink. Grow by double digits. Goldman CEO David Solomon called the selloff “too broad.” His own strategist Ben Snider warned of a “newspaper-like decline.” The narrative can’t hold itself together even within the same bank.

Jason Lemkin at SaaStr put it plainly: “The 2026 crash isn’t AI killing SaaS. It’s the market finally pricing in the deceleration that started in 2021.” Nobody is building a homegrown CRM in Replit.

What happened in 2021:

SaaS valuations peaked in November 2021. The median public cloud company traded at 17x forward revenue. Some hit 50x. Three things drove it: zero interest rates made future cash flows worth more today, COVID forced every company to buy remote-work software fast, and headcounts were growing.Seat-based pricing was a perpetual money machine.

Then the Fed raised rates in March 2022. Higher discount rates collapsed growth multiples overnight. Companies that over-hired in 2020–2021 ran mass layoffs in 2022–2023. Fewer heads meant fewer seats, which meant SaaS renewal conversations that used to be rubber stamps became uncomfortable. The Zylo stat (46% of licenses unused in any given month) isn’t an AI story. It’s the direct artifact of procurement decisions made when headcount projections were rosey-glassed.

By the time AI became the dominant narrative in 2024, the deceleration had been running for three years. The market needed a story that explained falling growth rates without admitting the original multiples were never justified.

AI is a convenient villain for a problem that started with a spreadsheet in 2021.

What’s actually dying

Per-seat pricing is dying. That much is real.

PricingSaaS tracked a 126% YoY surge in credit-based models: 79 companies now offer them, up from 35 at end of 2024. Figma, HubSpot, Salesforce have all moved. Gartner: by 2030, at least 40% of enterprise SaaS spend shifts toward usage-, agent-, or outcome-based pricing.

This isn’t software dying. It’s a billing model dying.

ELI5: Think about your kitchen blender. You didn’t just buy a blender — you built a smoothie habit around it. The recipes, the protein powder next to it, the morning routine. When someone says “AI will replace your blender,” they mean the appliance. Your dependency is on the workflow the appliance sits inside. Replacing the blender is easy. Replacing the habit, the integrations, the muscle memory — different problem entirely.

The average enterprise runs 305 SaaS applications. Zylo’s 2026 index: 46% of licenses go unused in any given month, costing $19.8M to $80.6M annually in shelf-ware.

There’s real fat to cut.

But cutting waste is a procurement exercise, not an existential reckoning.

The Klarna warning

The cautionary tale: Klarna. Their AI chatbot handled 2.3 million conversations in its first month: the workload of 700 agents. Headlines wrote themselves.

Then customer satisfaction fell. Hard.

Klarna started hiring humans back.

This is the pattern Post #12 identified. The headlines say “AI replaces 700 agents” and “company cancels SaaS contract.” What they skip is that the 20% of work that actually drives customer satisfaction (the edge cases, the judgment calls, the escalations) still needs a human. Klarna found that out the hard way.

Gartner thinks 35% of point-product SaaS tools get replaced by AI agents by 2030.

Point products — the single-purpose apps.

Your system of record with 14 integrations and a decade of compliance logic baked in? Much lower risk.

The distinction matters.

Faisal Hoque in Fast Company: enterprise software “encodes the enterprise itself”: decades of business rules, governance structures, compliance requirements.

You can clone the interface. The interface was never the product.

ELI5: It’s like saying “we replaced the filing cabinet with a scanner.” The cabinet is gone, sure. But the organizational system inside it (how things were labeled, who knew where to find what, the tribal knowledge of what goes where) didn’t transfer.

The cabinet cost $200. Re-creating the knowledge cost $200,000.

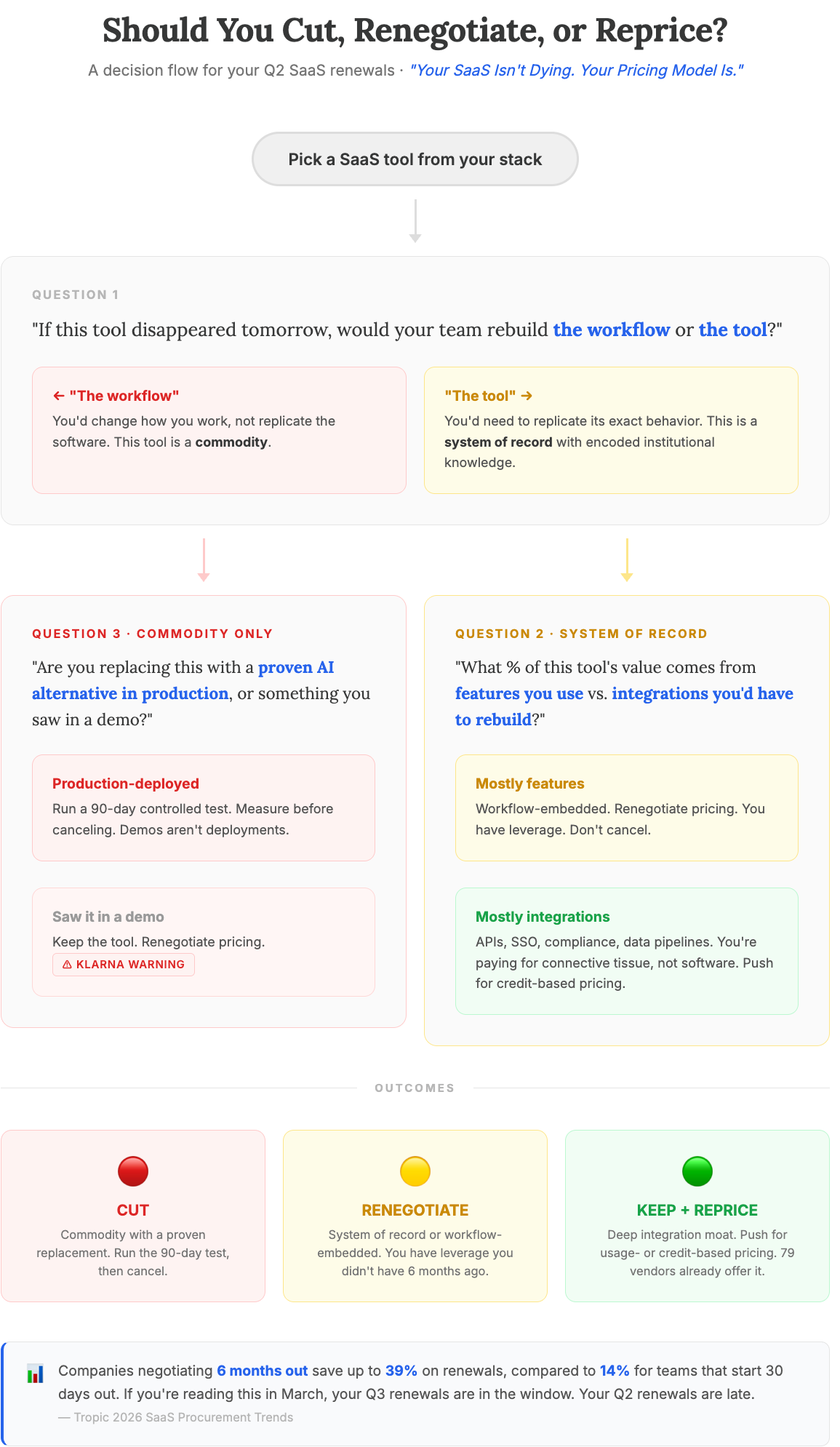

Three questions for your Q2 renewals

Before you cancel anything (or auto-renew without leverage), ask three questions:

“If this tool disappeared tomorrow, would my team rebuild the workflow or the tool?” If “the workflow” (meaning change how we work), it’s commodity. Replaceable. If “the tool” (meaning replicate its exact behavior), you’ve found a system of record with encoded institutional knowledge. Switching costs are real, and the AI replacement is years away, not quarters.

“What percentage of this tool’s value comes from features we use vs. integrations we’d have to rebuild?” The 54% of licenses still in active use often include deep integrations: APIs, single sign-on, compliance workflows, data pipelines. IDC: enterprises with 10+ integrations on a platform have 40% lower churn. If the answer is “mostly integrations,” you’re paying for connective tissue, not software. Renegotiate the price. Don’t cancel the contract.

“Am I replacing this with a proven AI alternative, or canceling based on something I saw in a demo?” The Klarna reversal is your cautionary tale. AI handles 80% of volume brilliantly and fails on the 20% that drives satisfaction and retention. If you can’t name a production-deployed AI alternative handling your specific workflow at enterprise scale today, renegotiate pricing (you have real leverage) and keep the workflow running while you evaluate.

In practice: A mid-market insurer cancels their contract management platform because “AI can draft contracts now.” Three months later, legal discovers 200+ custom clause templates and 14 compliance workflows were embedded in the old tool. Rebuilding takes 9 months. A Fortune 500 retailer renegotiates their CRM renewal at 30% below list. The vendor knows the alternative is cancellation, and the retailer knows they’re not actually canceling. A regional bank automates Tier-1 support with an AI agent, keeps the platform for escalation routing and compliance logging: spending less, not zero.

Companies negotiating six months out save up to 39% on renewals, compared to 14% for teams that start negotiations 30 days out (Tropic 2026). If you’re reading this in March, your Q3 renewals are in the window. Your Q2 renewals are late.

To be fair

There’s a version of this argument that’s too comfortable.

The “it’s just a pricing transition” thinking lets enterprise leaders exhale and go back to renegotiating contracts on familiar terms.

But the CEO staring at a portfolio of 305 SaaS tools should acknowledge something the cable TV analogy glosses over: in that transition, Blockbuster died and Netflix ate its business.

The aggregate market grew while individual companies got destroyed. Gartner’s 14.7% growth forecast doesn’t mean your specific vendor survives. It means the spend migrates to whoever figures out the new model first.

Renegotiate and pilot. Don’t exhale yet.

And the window for renegotiation assumes the vendor across the table will still be solvent when the contract renews.

For platform vendors with deep integration moats, that’s a safe bet.

For the point solution you’re paying $40K/year for?

Run the three questions. If the answer to question one is “rebuild the workflow,” you might be funding someone else’s runway.

What to do this quarter

This month:

Run those three questions across your SaaS stack. Tag each tool: system of record, workflow-embedded, or commodity. Consider cutting commodity. Renegotiate hard on systems of record.

Open renewal conversations for anything coming up in Q3. You have leverage you didn’t have six months ago.

This quarter:

Pilot credit-based pricing on one mid-tier platform renewal. 79 vendors already offer credit models. You’re not asking for something radical. You’re asking for what Figma and HubSpot already are offering.

Run one controlled AI replacement test on a tool you tagged as commodity. Measure for 90 days before canceling. Demos aren’t deployments.

The SaaSpocalypse isn’t an extinction event. It’s a pricing model transition, and that transition is creating real leverage for buyers. Your stack will change — that much is settled. Whether you’re driving it with data or reacting to a narrative written by people who don’t run your operations is the actual choice in front of you.

“Code is never where the value has lived.” — a16z

Which of your renewals this quarter are you renegotiating, and which are you actually ready to replace?

References: