The real SaaS killer isn't AI. It's the startups that never had per-seat pricing.

The company most vocal about “SaaS dissolves into agents” just launched a $99/seat bundle.

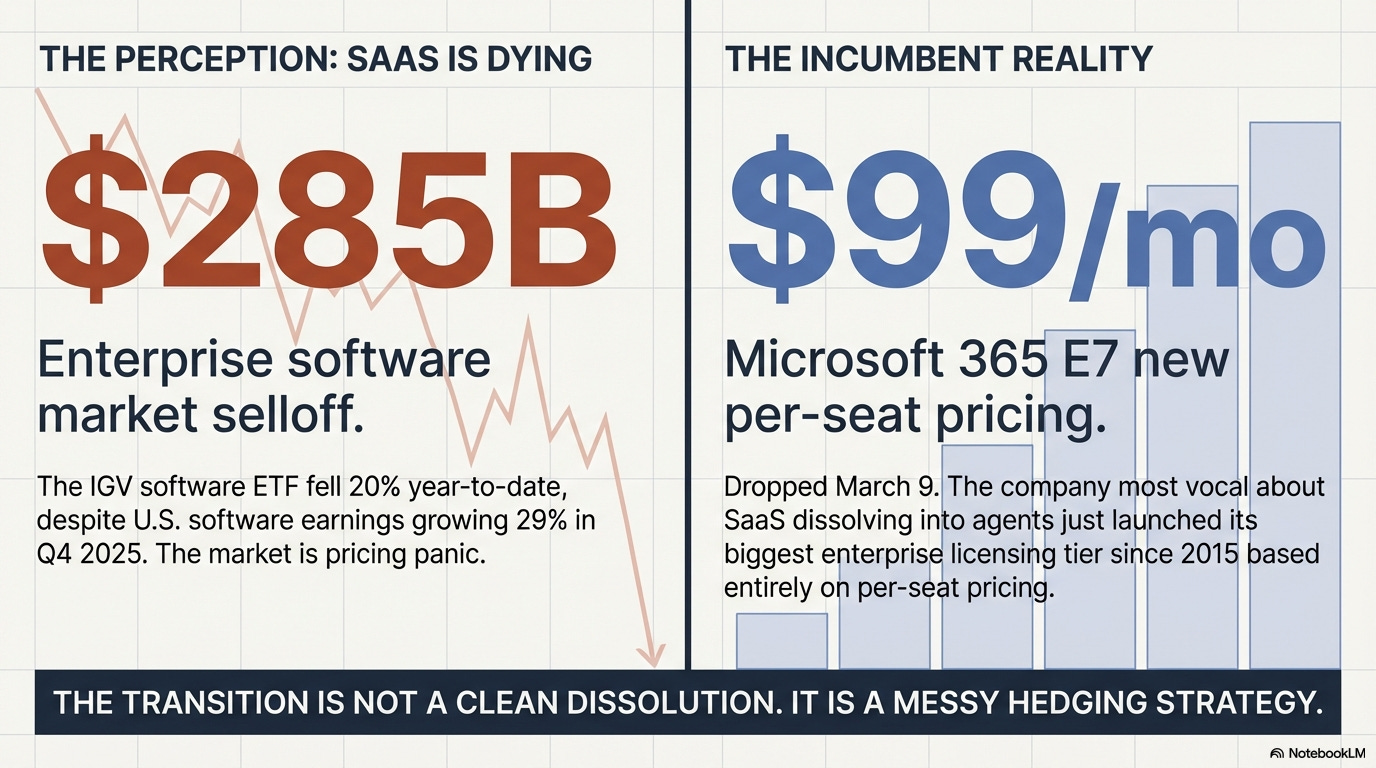

Microsoft 365 E7 dropped March 9. $99 per user per month. The biggest new enterprise licensing tier since E5 in 2015. Per-seat pricing. From the company whose CEO keeps saying SaaS will dissolve into agents.

A few weeks ago I wrote about the SaaSpocalypse — the $285B selloff and what it actually means for enterprise software. That piece got people talking, and two weeks of pressure-testing it sharpened the picture in three places. The thesis holds. But the threat model, the survival line, and the pricing transition are all messier than the perception that there is a clean narrative.

Time to add more definition.

The threat isn’t vibe-coders

Kian Katanforoush, who runs Workera’s AI skills assessments, said it plainly:

“Where is that vibe-coded Salesforce replacement? Who has used it? Nobody.”

A weekend project that replaces a login screen is not a product. Products have permissions, audit trails, integrations, and years of workflow logic baked into them.

But here’s what’s actually happening. Oro Labs closed a $100M Series C for AI-native procurement on March 12. 300% revenue growth, 150% net revenue retention, Fortune 500 clients including Coca-Cola and Pfizer. Translucent raised $27M for AI-native healthcare finance. Seventeen US-based AI companies raised $100M or more in the first two months of 2026. These aren’t weekend projects. They’re purpose-built systems that never had a per-seat model to begin with.

And then there’s Cursor. It hit $2B in ARR, adding roughly $1B in about three months. More than 64% of the Fortune 500 uses it. Salesforce reported that 90% of its 20,000 developers are on Cursor, driving 30%+ improvements in development velocity.

So no, some marketing manager’s Claude CRM isn’t the threat we should be watching. It’s well-funded, AI-native companies that skipped per-seat pricing entirely.

The survival line moved

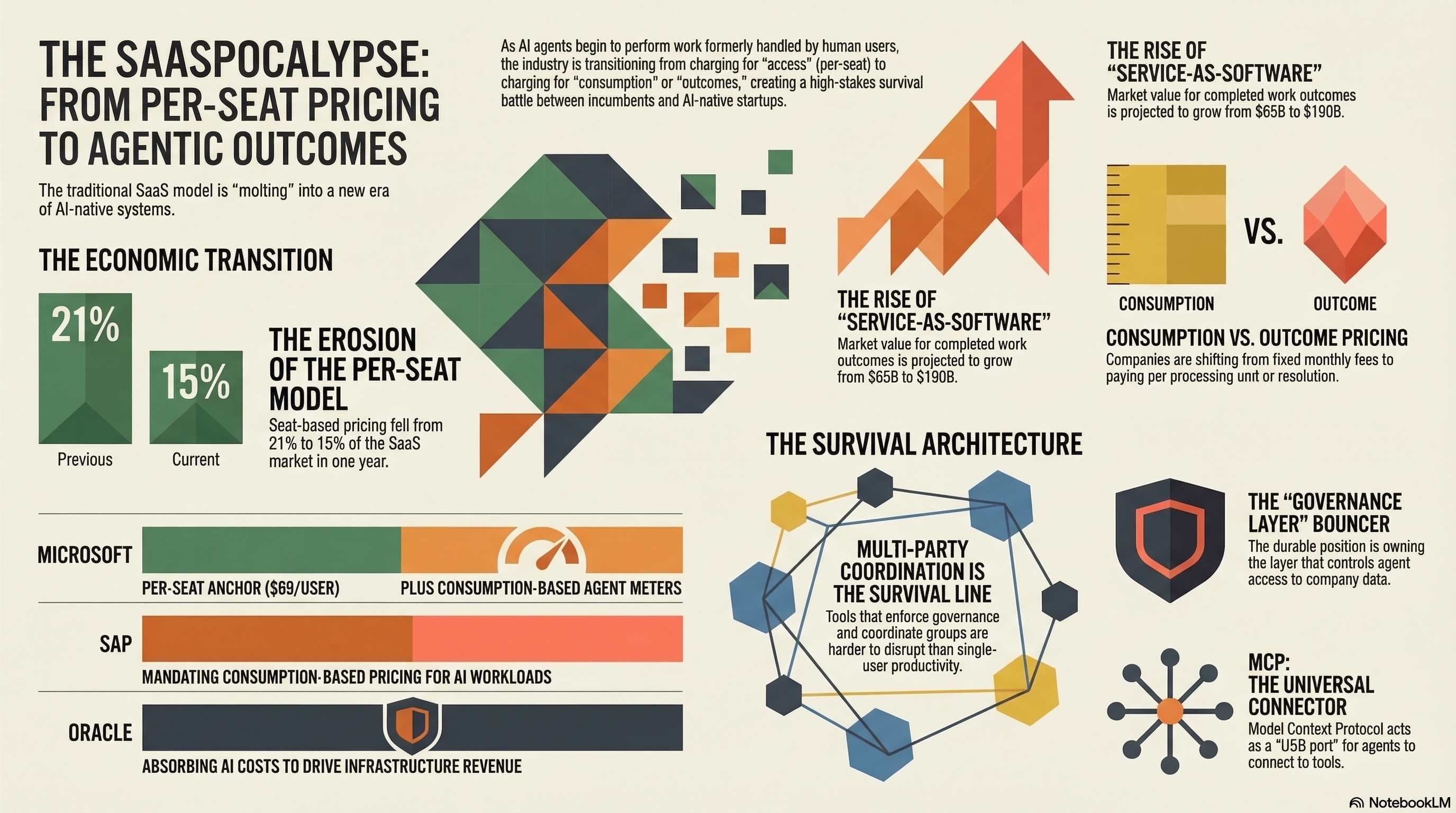

The split that matters is between multi-party coordination systems and single-user productivity tools. When Anthropic showed agents creating Excel and PowerPoint files without opening Office apps, SiliconANGLE flagged the implication: Nadella’s own thesis threatens Office most directly. If an agent can produce the spreadsheet, the slide deck, the report — the application becomes optional.

Systems that coordinate work between people and enforce governance? Much harder to dissolve.

Atlassian is showing what the survival playbook looks like. On March 12 they cut 1,600 jobs (10% of the workforce) while simultaneously embedding agents directly into Jira under existing permissions. Cut the people, embed the agents, keep the coordination layer. Not a contradiction — that is the strategy.

ELI5 — What’s MCP? Think of MCP (Model Context Protocol) as a USB port for AI agents. Before USB, every printer needed its own cable and driver. MCP is the standard plug that lets any AI agent connect to any enterprise tool (CRM, database, file storage) without custom wiring for each one.

The MCP 2026 roadmap published March 9 lays out the priorities: transport scalability, agent communication, and enterprise features like audit trails and SSO. OpenAI acquiring Promptfoo the same day (automated security testing and compliance for agent deployments) tells us where the value is going. OpenAI didn’t buy to make a better model. They bought the governance layer.

ELI5 — The governance layer: The rules and controls sitting between AI agents and our company data. Think of it as the bouncer at the door: checking who gets in, what they can touch, and logging everything they do. It doesn’t do the work. It decides whether the work is allowed to happen.

The EU AI Act’s high-risk compliance deadline hits August 2, 2026. Most of us don’t have a proper inventory of our AI systems yet. That governance gap is where the next enterprise software category gets harder to unplug.

The pricing picture got messy

This is where it gets really interesting.

Forrester’s latest data: seat-based pricing fell from 21% to 15% of the SaaS market in a single year. Hybrid and usage-based models surged to 41%. Chargebee reports 43% of companies now use hybrid pricing, projected to hit 61% by end of 2026.

ELI5 — Consumption vs. outcome pricing: Consumption-based is like the electric bill — we pay for kilowatt-hours, whether we left the lights on in an empty room or not. Outcome-based is like paying a contractor only when the house passes inspection.

SAP: consumption pricing for tools nobody loves yet

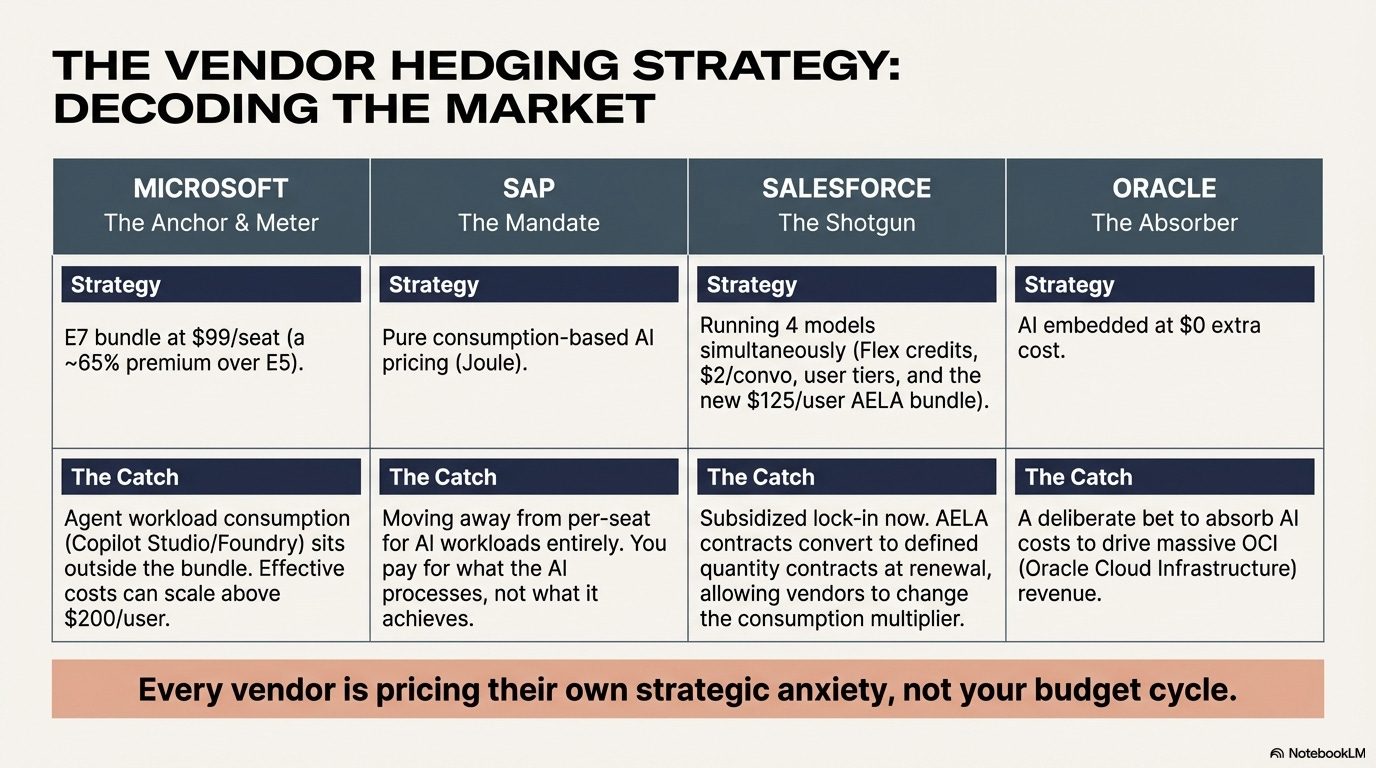

SAP CEO Christian Klein announced consumption-based AI pricing. The largest enterprise software company in Europe moving away from per-seat for AI workloads. Notice the word: consumption, not outcome. We pay for what the AI processes, not what it achieves. This came three weeks after Bloomberg reported SAP customers calling Joule “difficult to use, limited and not worth the price.” Consumption pricing for tools customers aren’t sold on yet. That’s a specific kind of bet.

Salesforce: four models and counting

Salesforce is running four pricing models simultaneously: Flex Credits, $2/conversation, per-user tiers from $5 to $550/month, and the new Agentic Enterprise License Agreement (AELA), bundling unlimited Agentforce, Data Cloud, and MuleSoft starting around $125/user/month. CRO Miguel Milano said Salesforce is “OK with losing money on some AI deals.” Sounds generous until you read Gartner analyst Hannah Decker’s warning that AELA contracts “will be converted into defined quantity contracts at the end of the agreement.” The vendor can change the consumption multiplier at renewal. Subsidized lock-in now, monetization later.

Oracle and the mid-tier hedgers

Workday and ServiceNow ($600M ACV) are hedging with bundled credits. Oracle co-CEO Mike Sicilia said on the March 10 earnings call: “We are the disruptor because we are actually embedding the AI right into our applications, full stop, at no additional cost.” Oracle absorbs the AI cost and bets on OCI infrastructure revenue instead.

Microsoft: the $99 anchor with a hidden meter

And then there’s Microsoft. E7 bundles Copilot, Agent 365, and the full security stack at $99/seat, roughly a 65% premium over E5, based on analyst estimates. But agent workload consumption through Copilot Studio and Microsoft Foundry sits outside that $99. Some analyst estimates put agent-heavy Microsoft deployments above $200/user/month in effective cost. The per-seat price is the anchor. The consumption meter runs alongside it.

In practice: Say we’re renewing enterprise agreements this quarter. Microsoft gives us a predictable $99/seat number the CFO can model. SAP tells us to budget based on AI consumption nobody can forecast. Salesforce offers four pricing structures depending on which sales team we talk to. Oracle says AI is free, but the infrastructure bill is climbing. Each vendor is pricing its own strategic anxiety, not our budget cycle.

Here’s what jumped out at me: every vendor is hedging, except SAP (mandating) and Oracle (absorbing). And the strongest per-seat commitment came from the company most vocal about the agent thesis. Microsoft!

The productivity evidence isn’t helping

The productivity case isn’t settling it either. Goldman Sachs found no meaningful relationship between AI adoption and productivity economy-wide. Deloitte’s 2026 State of AI: 74% of organizations want AI to grow revenue, only 20% have seen it happen. McKinsey: 88% deploying AI, 1% calling their strategy “mature.” So the industry is asking us to move from a pricing model we understand to one nobody can define yet, and the productivity evidence stays mixed.

And we’ve seen this movie before. Adobe’s perpetual-to-subscription shift took the better part of a decade. Microsoft still sells perpetual Office licenses fifteen years into 365. Pricing model transitions in enterprise software don’t end cleanly. The messy middle sticks around longer than anyone budgets for.

To be fair

Every vendor running multiple pricing models might be doing exactly the right thing.

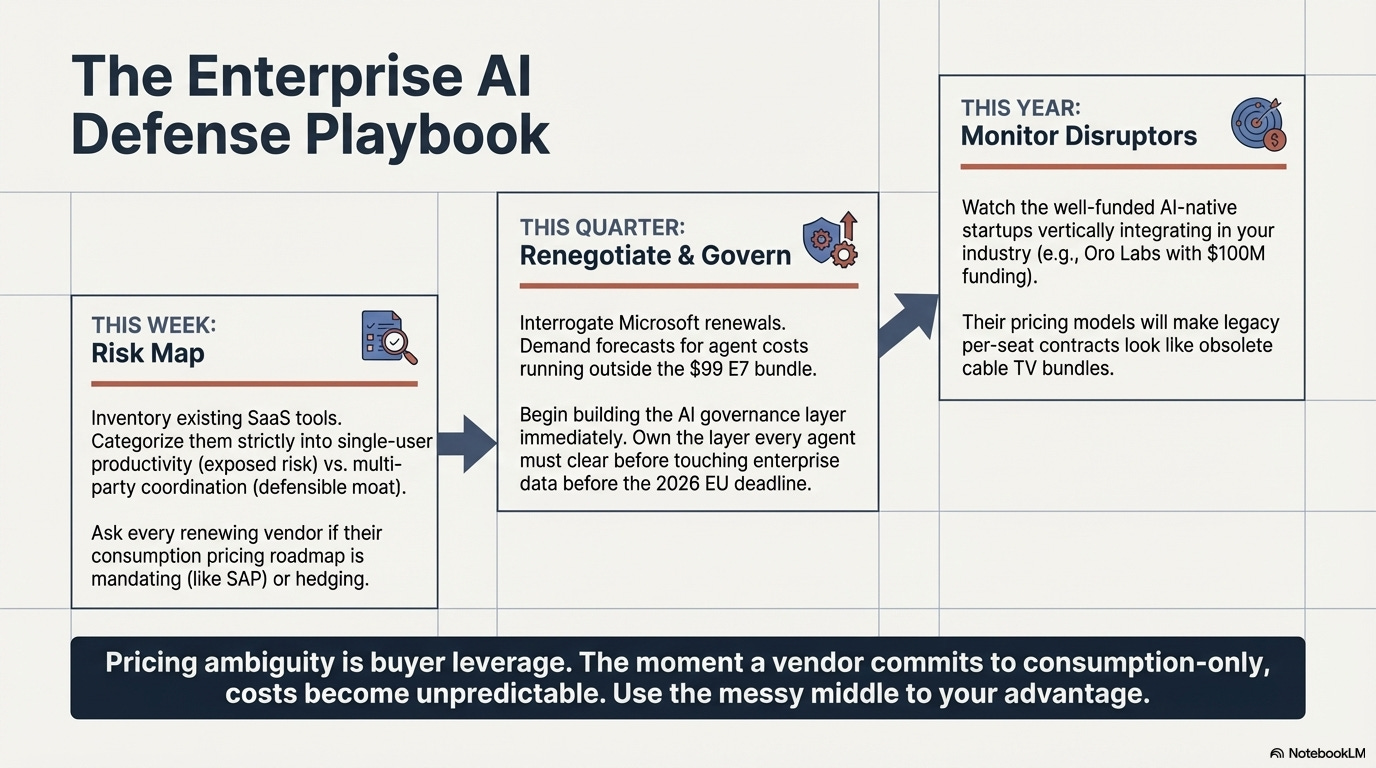

From the buyer’s side, pricing ambiguity is leverage. The moment a vendor commits to consumption-only, our costs become variable and our budget forecasts get harder, which is exactly the unpredictability that SaaS subscriptions were invented to solve.

The incumbents are doing fine. On March 10, Deutsche Bank upgraded enterprise software to Overweight, declaring AI disruption fear has reached “capitulatory peak.” U.S. software earnings grew 29% year-over-year in Q4 2025, but the IGV software ETF fell 20% year-to-date. Not a single software company expects a negative revenue effect from AI in 2026. The stock market is pricing panic. The earnings statements are pricing growth.

And the governance layer argument is real, but building it now means coupling to protocols that are still publishing their own roadmaps. Sometimes the right move is to wait. Not because we’re behind, but because the foundation hasn’t set yet.

So what do we do with this?

The original thesis holds. The specifics are sharper now. And there’s a name for what comes next: PitchBook’s Q1 2026 analyst note calls it “Service-as-Software” — vendors selling completed work outcomes instead of tool access. $65B market today, $190B by 2030. Intercom’s Fin is the proof point everyone keeps citing: $0.99 per resolved ticket, eight-figure ARR, 393% annualized growth. SaaS isn’t dying. It’s molting into something with different economics.

In practice: Say our help desk incumbent charges $50/seat/month for 200 agents. Intercom Fin offers $0.99 per resolved ticket. At 15,000 tickets/month, the math works — but only if “resolved” means actually resolved, not just “responded to.” The definition of the outcome becomes the new negotiation battleground.

This week: Inventory which SaaS tools are single-user productivity (exposed) versus multi-party coordination (defensible). That’s the risk map. Ask every renewing vendor about their consumption pricing roadmap — are they mandating or hedging?

This quarter: Ask the Microsoft rep what happens to costs when agents run outside the E7 bundle. Ask Salesforce which of their four pricing models they’re betting on in five years. Start building the AI governance layer. Not because regulators arrive August 2, but because the coordination layer between our agents and our data is the only durable position.

This year: Watch the AI-native startups in our verticals. The threat isn’t the team vibe-coding a replacement. It’s Oro Labs with $100M in funding and a pricing model that makes our per-seat contracts look like cable TV bundles.

The durable position isn’t surviving the pricing shift. It’s owning the layer every agent has to clear before it touches enterprise data.

What’s your vendor telling you about consumption pricing?

And, honestly do you believe them?

Additional references (not linked inline):