The Pruning, the Symbiosis, and the Speciation: three bets companies are making about humans in the AI era

What does Evolutionary Biology has to do with IT Operating Models?

In the same quarter Cloudflare cut 1,100 roles in an AI-driven restructuring, it hired 1,111 paid summer interns, picked out of roughly a million applications, all labeled “Builders” or “Sellers.”

One company. Near-identical numbers.

Two opposite bets about what AI does to the humans inside it.

That math is what caught my eye.

The AI restructuring debate jams four bets together at once:

cutting costs,

getting more done with the same team,

building new abilities, and

reinventing what the company sells.

The bet about humans is the one driving the other bets. Three answers are visible in the wild. Each is a different bet on how humans evolve when AI shows up.

The real question is which combination matches the company you actually have.

What does Evolutionary Biology has to do with IT Operating Models?

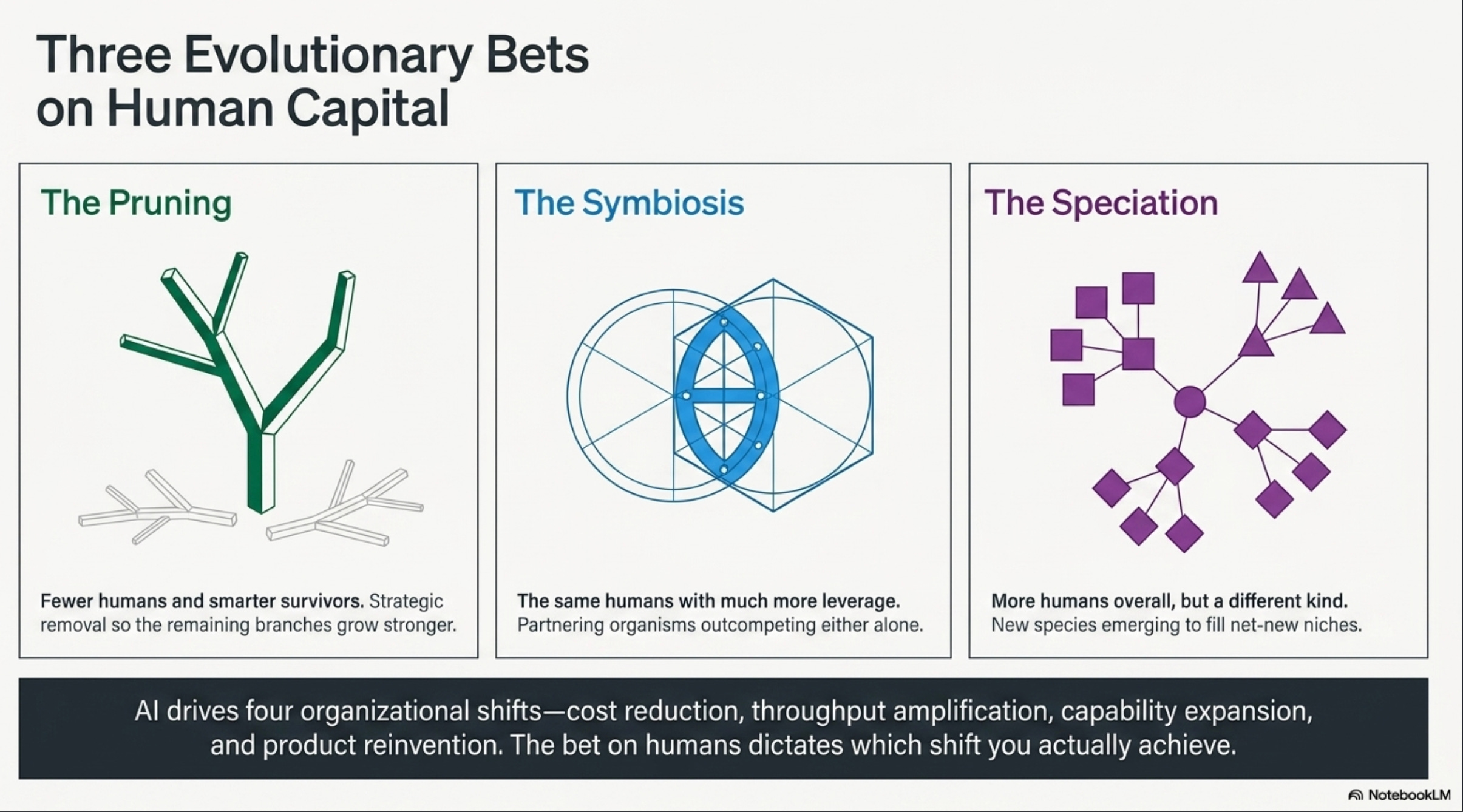

I’m going to call them The Pruning, The Symbiosis, and The Speciation. Borrowed from evolutionary biology because borrowing from McKinsey gives you another exhausted “3 horizons” diagram nobody believes.

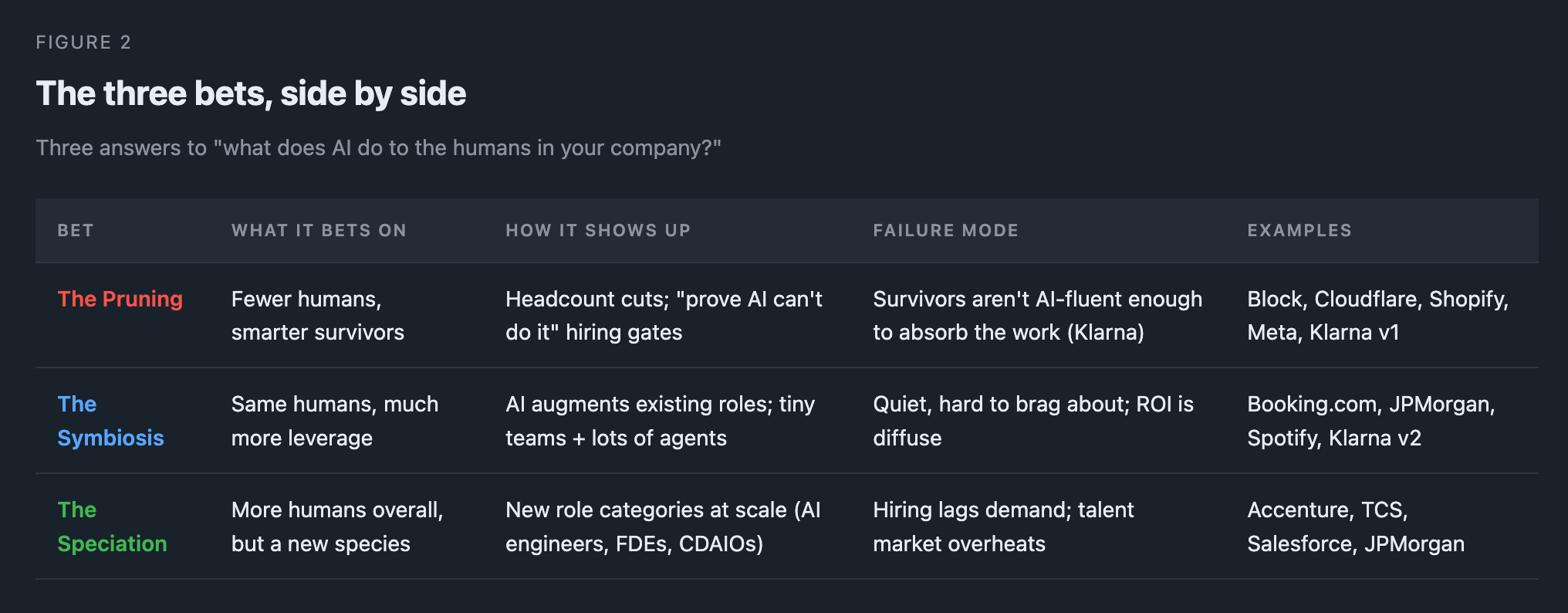

The Pruning bets on fewer humans and smarter survivors. Cut strategically so the branches that remain grow stronger.

The Symbiosis bets on the same humans with much more leverage. Two organisms team up; each does what the other can’t; together they beat either one alone.

The Speciation bets on more humans overall, but a different kind. New species emerge to fill new niches.

ELI5: What do these three biology terms mean, and why borrow them?

Pruning is what a gardener does to a tree. Cut branches strategically so the remaining ones get more light, water, and nutrients. The tree gets smaller on purpose, and what’s left grows stronger. It’s not “less tree” — it’s a more concentrated tree.

Symbiosis is what happens when two different species live together and both win. Clownfish and sea anemone: the fish hides inside the anemone’s stinging tentacles for protection from predators, and in return cleans the anemone and chases off its competitors. Neither pulls it off alone. (Bees and flowers, oxpecker birds and rhinos — same pattern.)

Speciation is how one ancestor species splits into several distinct species over time, each adapted to a niche the original couldn’t fill. Darwin’s finches in the Galápagos are the textbook case: same ancestor, different beak shapes for different food sources. New species filling new niches because the environment opened them up.

Why borrow from biology instead of business terms?

Each of these is a different evolutionary response to the same environmental pressure. That matches what AI is to companies right now: a new force in the environment, and three different ways to adapt to it. Business-strategy frameworks treat the choice as a deliberate plan you sit down and pick. Biology treats it as a fit-to-environment problem, where what works depends on what you already are. The biology framing is more honest about how little control any single company has over the pressure itself — and how much depends on the starting conditions you actually inherited.

This is a debate about what kind of evolutionary pressure you think AI is.

The three answers are observable in the corporate wild right now.

The choice between them is shaped by five things:

how AI-fluent your people already are,

how much freedom you have to redesign governance,

how easily you can move headcount,

how much risk you can swallow, and

how patient your investors are.

I’ll come back to those at the end. Cases first.

At this point, I’m not recommending a bet. I’m naming what companies are actually doing, and giving the labels enough light shone on them.

The Pruning

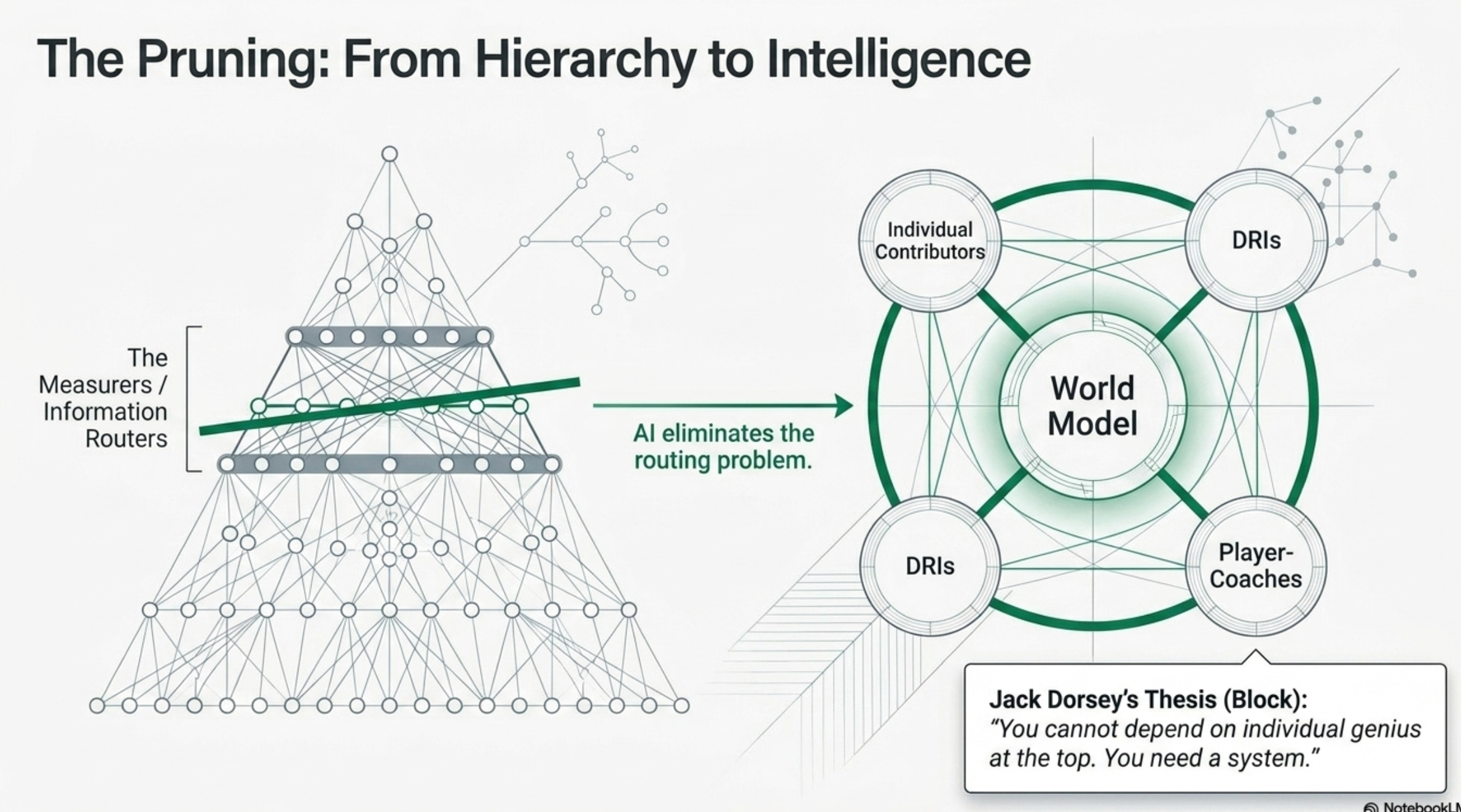

The cleanest take on The Pruning is a March 31, 2026 essay by Jack Dorsey and Roelof Botha, published jointly on Sequoia Capital and Block’s own channels, titled From Hierarchy to Intelligence.

The argument: managers exist because information has to be routed. AI handles the routing now. So the manager-as-information-traffic-cop can go.

What’s left is three roles (Individual Contributors, Directly Responsible Individuals, and Player-Coaches) coordinating around a company-wide “world model” that records every decision, plan, problem, and progress update.

ELI5: What’s a “world model” in this context?

Think of it as the company’s shared, always-current Wikipedia plus task list plus decision log, except it’s written by AI from everything happening across the business. Anyone (and any AI agent) can ask it, “What’s the status of X?” and get a usable answer without going through a chain of managers.

Dorsey’s words: “You cannot depend on individual genius at the top. You need a system.”

The argument is basically this: the Roman legion was strong because its protocol for moving information up and down the line was unusually good for its era, not because any particular centurion was brilliant.

Replace the centurions with the world model and you get a flatter org that moves faster.

The essay arrived weeks after Block already executed against the thesis. The company cut roughly 40% of its workforce, over 4,000 roles, in February 2026, bringing headcount just under 6,000.

Dorsey’s prediction in the shareholder letter coverage: “Within the next year, I believe the majority of companies will reach the same conclusion and make similar structural changes.”

Cloudflare’s Matthew Prince ran the same bet at a finer grain. In a Wall Street Journal op-ed published May 21, 2026,

Prince split every employee into three buckets:

Builders (who make the product),

Sellers (who sell it), and

Measurers (his term for middle management, finance, legal, internal auditing, and revenue recognition).

His claim: “The vast majority of those we laid off last week were measurers.” AI, he argued, can now do measurement work with an objectivity and tirelessness humans never could.

The numbers behind this premise are real. On its Q1 FY26 earnings call (May 7, 2026), Cloudflare said 97% of engineers in R&D use AI coding tools and internal AI usage grew 600% in three months.

Shopify’s Tobi Lütke posted his “AI-first” memo on X on April 7, 2025, a year before Cloudflare and Block went public with theirs. Shopify made it a procedural requirement.

Before asking for more headcount, teams have to show that AI can’t do the work. The memo’s signature phrase: “Reflexive AI usage is now a baseline expectation.” Headcount fell from 11,600 in 2022 to about 8,100 by the end of 2024 (close to a 30% cut) while revenue grew north of 20% per year, per CNBC’s coverage of the memo.

Meta is the loudest current example.

In April 2026 the company reorganized its AI work under Alexandr Wang’s new Meta Superintelligence Labs, then announced 8,000 layoffs on April 19, roughly 10% of the workforce, to be executed by May 20.

On the same Q1 FY26 earnings call, Meta raised its 2026 capex guidance to $125–$145 billion from a prior $115–$135B band, nearly double FY25 spend.

The wording matters: the cuts and the capex raise are the same bet. Payroll dollars in non-AI functions are being converted into infrastructure dollars to staff the AI ones. AI work has become important enough inside Meta to be funded from inside, even if it means visibly under-staffing other functions.

ELI5: What’s capex?

Capex is short for capital expenditure: long-lived investments like data centers, chips, and buildings, as opposed to ongoing costs like salaries. When Meta says “$125–145B in capex,” they mean physical AI infrastructure: GPUs, servers, the buildings around them. It’s the bill for the AI arms race.

The Pruning has a cautionary tale, and it’s Klarna.

Through 2023 and 2024 the company publicly celebrated an AI customer-service bot that, by its own framing, “did the work of 700 customer service agents,” alongside a year-plus AI-driven hiring freeze.

Headcount fell from about 5,000 to roughly 3,000. Then, in a Bloomberg interview on May 8, 2025, CEO Sebastian Siemiatkowski reversed course. He did not use the phrase the headlines later attached to him. His actual words: “As cost unfortunately seems to have been a too predominant evaluation factor when organizing this, what you end up having is lower quality.” And: “From a brand perspective, a company perspective, I just think it’s so critical that you are clear to your customer that there will always be a human if you want.”

Klarna started hiring back, on an Uber-style remote-agent model, and Siemiatkowski later warned on CNBC’s Power Lunch (May 14, 2025) that the workforce had shrunk by 40% and that other CEOs were “sugarcoating” AI’s labor impact.

The Pruning works when the survivors are AI-fluent enough to absorb the workload. Klarna shows what happens when the judgment work underneath (which model handles which case, when to escalate, what tone to use on a disputed charge) was never AI-ready to begin with.

The Symbiosis

The Symbiosis bet is the quietest of the three because it doesn’t generate layoff press releases. The flagship case is Booking.com, and it’s the flagship because the architecture predates the “AI agents” buzzword by several years.

At QCon London in March 2026, Booking’s Senior Principal Engineer Jabez Eliezer Manuel walked through the production architecture: more than 480 machine-learning models running live, producing roughly 400 billion predictions per day, each in under 20 milliseconds.

The setup has three layers:

small specialist models for speed,

large reasoning models for trust-critical paths, and

a judging layer that decides which model handles what.

VentureBeat’s coverage summarized the design as small models for speed, large models for trust. Human travel-domain specialists supervise the judging layer. The humans haven’t gone away. They’ve moved one level up: from doing the routing themselves to telling the system how routing should work.

JPMorgan’s LLM Suite is the same bet at a bigger bank. Per CNBC’s September 30, 2025 feature, the firm’s internal AI front-door makes wealth advisors find information 95% faster, improves fraud detection by 40%, and ships new data sources and tool integrations every 8 weeks.

American Banker named it 2025 Innovation of the Year. Estimated annual value across JPMC’s AI portfolio sits between $1.5 and $2 billion, depending on how you count infrastructure.

None of the wealth advisors got laid off.

A senior advisor who used to spend twenty minutes pulling research can now spend twenty seconds. The freed-up hours don’t disappear; they get redeployed into more client coverage.

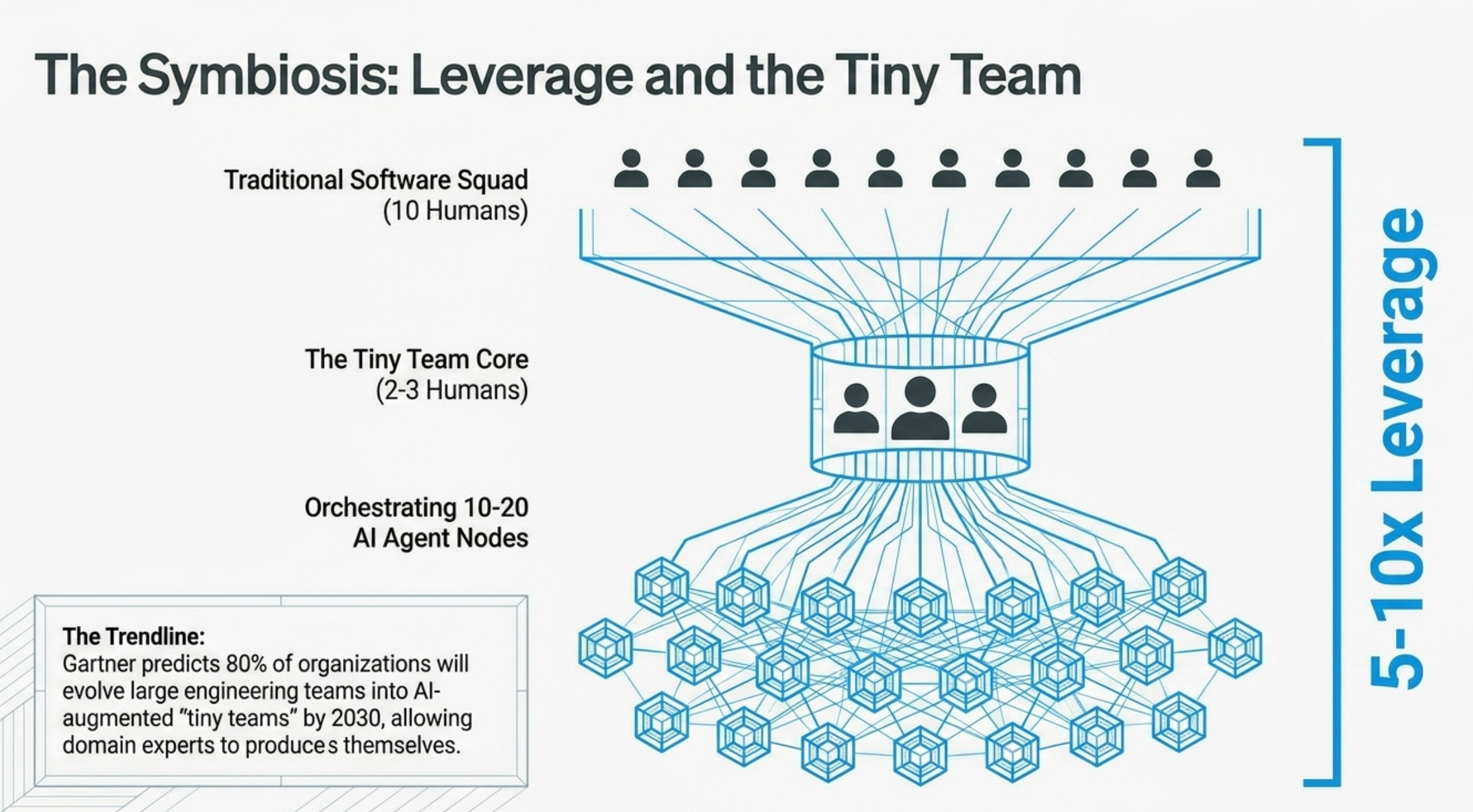

Spotify needs a caveat before I cite it. People watching from outside (and CIO.com’s September 2025 piece sums it up best) describe the new Spotify squads as 2 to 3 humans plus 10 to 20 AI agents, getting 5 to 10 times the output of the old all-human squad. That ratio comes from outside writers; Spotify itself hasn’t published it. I’m including it because the same pattern shows up across other product teams I watch.

Treat the exact numbers as outside guesses for a shift Spotify hasn’t confirmed on its own.

The bigger trend is easier to defend. Gartner’s October 20, 2025 trends release for 2026 predicted that by 2030, 80% of companies will shrink large engineering teams into smaller, AI-augmented “tiny teams.”

“Leading organizations are creating tiny platform teams to allow non-technical domain experts to produce software themselves, with security and governance guardrails in place.”

The Symbiosis bet keeps the engineer. It changes what a productive team even looks like.

The under-told piece of the Klarna story sits here, in Symbiosis. Per Bloomberg’s September 10, 2025 reporting, Klarna built a new AI-cloned-CEO customer-service hotline where AI handles the intake and humans handle the resolution.

Klarna pivoted from pure Pruning to Symbiosis.

The bot triages; the human closes out. The bet about humans changed; the bet about AI didn’t.

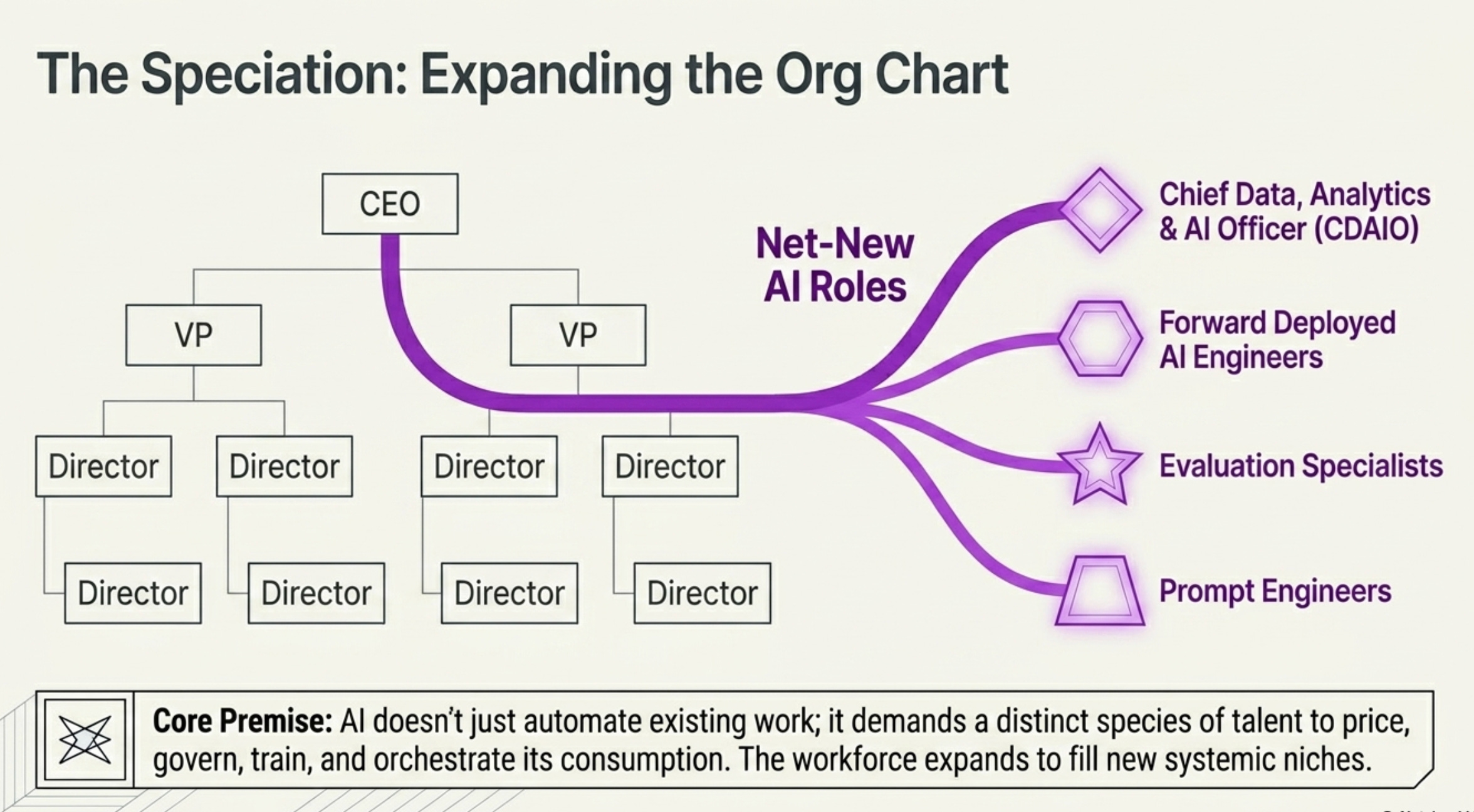

The Speciation

The Speciation bet doesn’t show up in layoff coverage because it’s a “we created new roles” story, not a “we cut old roles” story.

JPMorgan’s same CNBC feature documents roughly 1,700 AI specialists supporting 450+ live models on that 8-week deployment schedule. The number isn’t a reshuffle of the existing engineering team. It’s a category (AI/ML engineers, prompt engineers, evaluation specialists, governance leads) that didn’t exist at scale inside the bank three years ago. Estimated annual value contribution: $1.5–$2 billion across the AI portfolio. The same article that supports the Symbiosis bet on wealth advisors is also the cleanest evidence for Speciation.

Same company, same article, two bets.

Accenture launched a Forward Deployed Engineering program with ServiceNow on May 6, 2026, pairing ServiceNow AI-native engineers with industry-experienced Accenture engineers inside customer environments. That’s a brand-new joint role category that didn’t exist in 2024.

ELI5: What’s a Forward Deployed Engineer?

Originally Palantir’s invention. An engineer who literally lives inside the client’s office, works on their problem with their data, and ships fixes in days instead of writing a six-month consulting deck. It’s the consultant-engineer hybrid that vendors increasingly use to make AI products actually land in real companies.

That FDE program sits on top of a much bigger hiring push. Accenture grew its AI and data staff from roughly 40,000 in fiscal 2023 to nearly 77,000 in fiscal 2025, almost doubling in two years, per Computer Weekly’s read of Accenture’s investor filings. In fiscal 2025, Accenture signed $5.9 billion in new AI contracts (double the prior year) and pulled in $2.7 billion in AI revenue (triple the prior year). The $1 billion LearnVantage training program announced in early 2024 paid for the training side.

The bet here: AI demands a new species of consultant, and Accenture is hiring and training that species fast.

TCS is running the same bet from a different starting point.

Per the firm’s Q3 FY26 press release (January 2026), AI services now generate $1.8 billion in annualized revenue, up from $1.5 billion at the December 2025 Analyst Day, with 17.3% growth quarter over quarter in constant currency.

Krithivasan’s own framing:

“Our AI services now generate $1.8 billion in annualized revenue, reflecting the significant value we provide to clients through targeted investments across the entire AI stack, from infrastructure to intelligence.”

Behind the revenue number: 54 of TCS’s top 60 clients running major AI projects, 5,500+ AI projects delivered globally, and 180,000+ employees trained in advanced AI skills.

TCS is building a different delivery model, and staffing it with a different kind of person.

Salesforce is the Speciation bet on the vendor side.

Per the Q4 FY26 earnings release on February 25, 2026, Agentforce reached $800 million in annual recurring revenue, up 169% year over year, with 29,000 deals closed since launch and combined Agentforce + Data 360 annual recurring revenue at $2.9 billion.

Marc Benioff’s framing:

“Agentforce ARR reached $800 million, up 169% year-over-year, and we’ve closed 29,000 deals, up 50% quarter-over-quarter.”

The structural shift here (my interpretation, not Salesforce’s) is that selling agents as a metered service is a different motion than selling seats. The sales org has to learn to price agent runtime, control what agents are allowed to do, and renew on usage rather than license counts. Whatever you want to call that role, it didn’t exist in the same shape two years ago.

ELI5: What’s ARR?

Annual Recurring Revenue. The yearly run-rate of subscription revenue. If a customer pays $100/month, that’s $1,200 of ARR. SaaS companies report it because it tracks the underlying contracted business better than calendar-quarter revenue. Agentforce’s $800M ARR means contracts currently on the books are set to generate $800M/year.

The pattern goes all the way to the C-suite.

HBR’s December 2025 piece by Vipin Gopal, Tom Davenport, and Randy Bean argues that the combined Chief Data, Analytics, and AI Officer (CDAIO), also titled Chief AI Officer in some shops or AI-augmented Chief Risk Officer in regulated finance, is now an emerging norm in how companies organize the top.

The Data & AI Leadership Exchange’s 2025 survey, cited in the HBR piece, finds that 33.1% of organizations have appointed a new AI leader. The Federal Reserve has appointed a Chief AI Officer focused on supervisory and risk-management dimensions; the OCC, Federal Reserve, and FDIC jointly issued revised Model Risk Management guidance on April 17, 2026 (Bulletin 2026-13) reflecting how central AI-model governance has become at the federal supervisory level.

A role that didn’t exist three years ago is now a regulator-recognized job title.

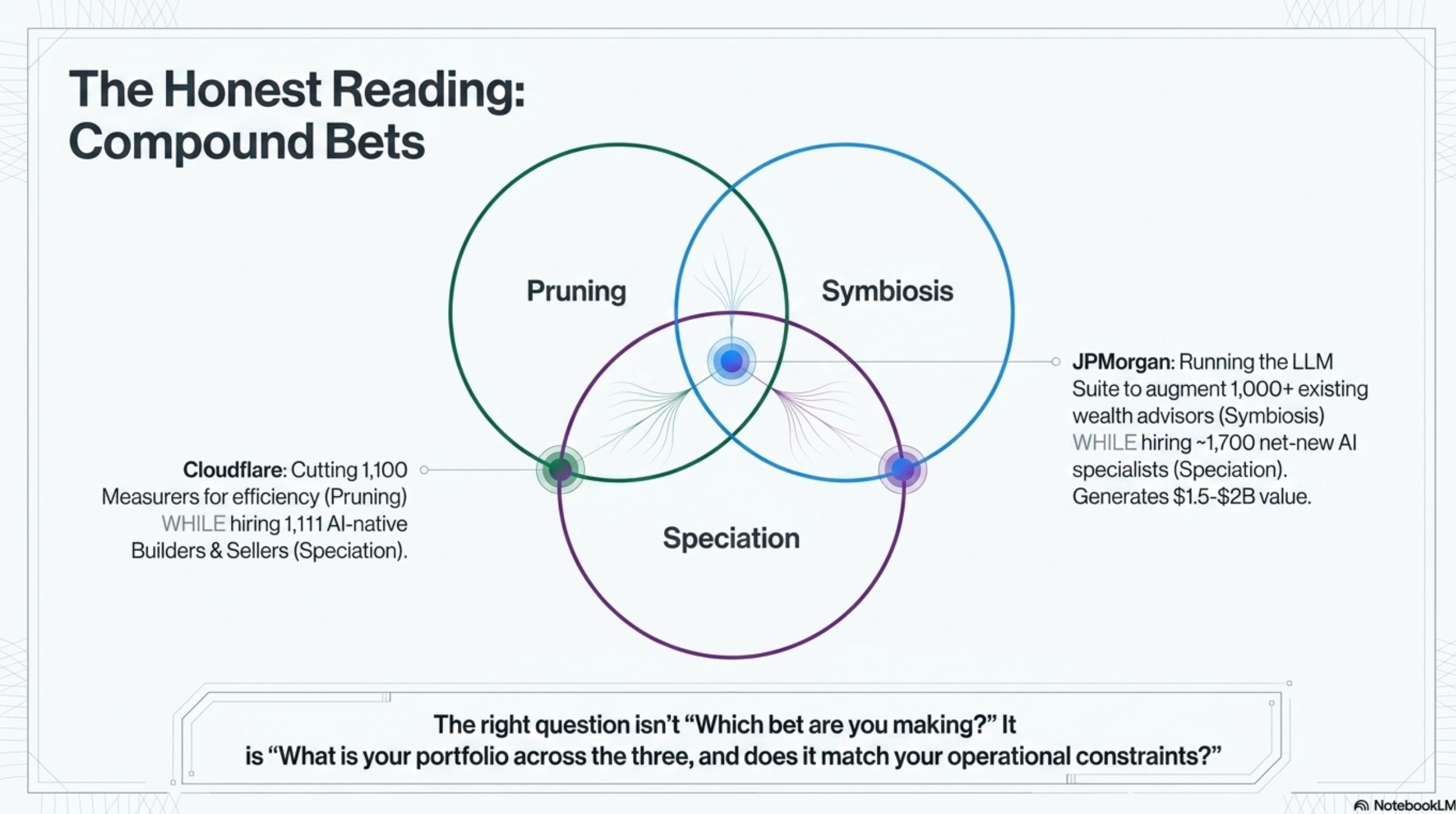

The honest reading

Most companies are placing more than one bet at once.

JPMorgan is doing both Symbiosis (LLM Suite making 1,000+ wealth advisors faster) and Speciation (~1,700 AI specialists, a brand-new role category)

Cloudflare is doing both Pruning (1,100 Measurers cut) and Speciation (1,111 AI-native interns hired, all Builders and Sellers). Same company. Same quarter. Two bets running side by side.

That’s what serious AI adoption actually looks like. The better question: what mix of the three are you running, and does it fit the company you actually have?

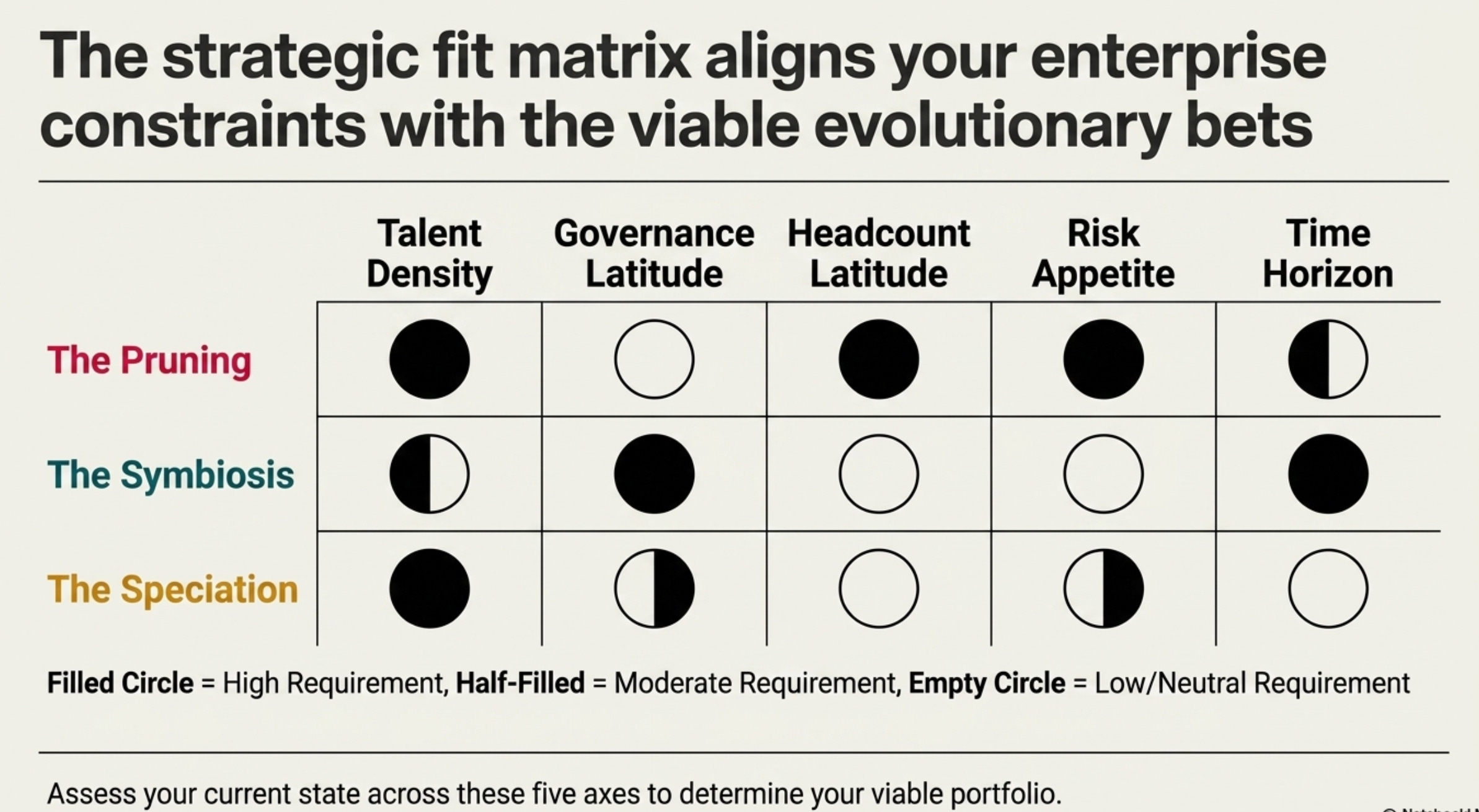

The 5 constraints we should watch for:

How AI-fluent your people already are. Cloudflare’s 97% AI-tool usage among engineers (Q1 FY26 earnings call) is the saturation level that makes a Pruning bet survivable. A company with 30–40% usage cannot prune the same way; the survivors won’t absorb the workload.

How much freedom you have on governance. The Block thesis assumes you can wire up the entire company on a “world model” that records every decision; few regulated companies (insurance, healthcare, EU-located firms) have that kind of unified authority over their own data.

How easily you can move headcount. Meta could reassign 1,000 engineers and cut 8,000 elsewhere inside a single quarter, partly because US at-will employment plus generous stock-comp severance pools absorb the friction. European companies with works-council seats (worker representatives with veto rights on big restructurings) can’t move at that speed.

How much risk you can swallow. Klarna is the documented public failure of a pure Pruning bet. The cost of being wrong was twelve-plus months of brand damage plus a workforce rebuild. Thinner-margin businesses might not survive that.

How patient your investors are. JPMC’s LLM Suite shows Symbiosis payoff inside year one; Salesforce shows Speciation payoff inside one product cycle (though the payoff goes to the vendor, not the customer); Block’s Pruning shows immediate impact on the income statement, but the “we move faster now” thesis won’t be testable until roughly Q1 2027.

I’m deliberately not recommending a mix. The AI-and-headcount question doesn’t have a right answer; it has a fit answer, and the five things above are the constraints that determine fit. Read your own company against them, then decide where on the spectrum you actually sit.

Close

The debate will keep treating Pruning, Symbiosis, and Speciation as competing strategies. The people figuring this out fastest are running combinations of all three, sized to the constraints they actually have rather than the strategy they wish they did.

Pick the bet that matches the company you actually have. Pick the mix that matches the future you can actually staff.