AI Waypoints — Week of May 4, 2026 — Edition #8

The biggest enterprise AI procurement constraint of the last three years just broke open. Plus Agent 365 GA, Pentagon's Anthropic freeze, and the EU AI Act's 90-day clock.

Good morning. The single biggest enterprise AI procurement constraint of the last 3 years that OpenAI meant Azure — broke open this week, and the rest of the week shifted around it. 3 of this week’s 8 signals touch Microsoft; and I try real hard not to be biased towards one sector!

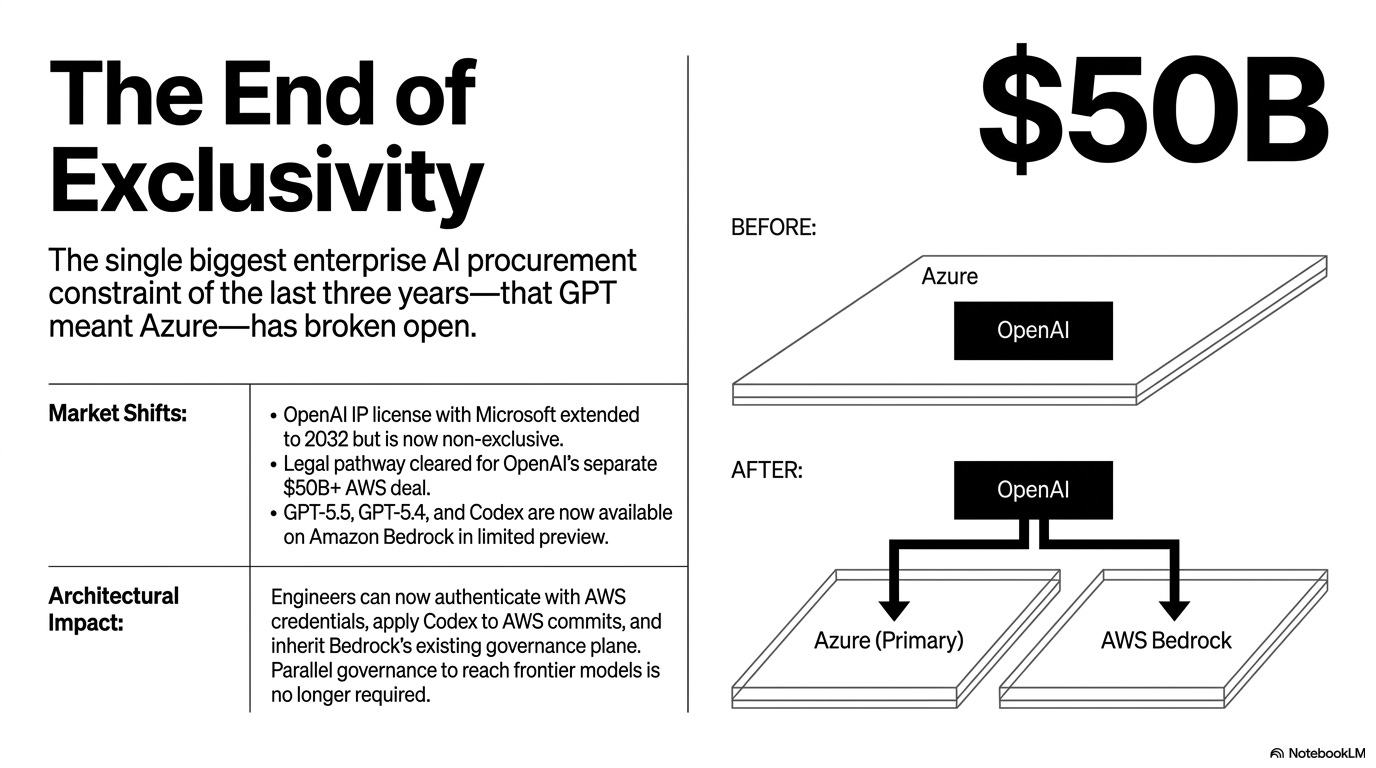

1. Microsoft and OpenAI restructure ends Azure exclusivity

What happened: On April 27, Microsoft and OpenAI jointly announced an amended partnership. Microsoft’s IP license extends through 2032 but is now non-exclusive. OpenAI can ship products on any cloud, with Azure remaining “primary,” first when feasible, not exclusively. The AGI clause is gone, and the legal path opened for OpenAI’s separate $50B+ AWS deal the very next day.

Why it matters: Procurement teams potentially spent two years standardizing on Azure purely to access GPT. That constraint is gone. Multi-cloud AI strategies that were theoretical 6 months ago are operational, and negotiating leverage with Microsoft just shifted.

What to do: Ask procurement and architecture leads two things this week. -

Where did you choose Azure primarily for OpenAI access, and what would you change if that constraint vanished?

Do you want OpenAI workloads behind AWS Bedrock’s governance plane, Azure’s, or both?

2. OpenAI ships GPT-5.5 and Codex on AWS Bedrock

What happened: One day after the Microsoft restructure, OpenAI made GPT-5.5 and GPT-5.4 available on Amazon Bedrock in limited preview. Codex was available on AWS the same day, alongside a Bedrock Managed Agents product powered by OpenAI. Customers authenticate with AWS credentials, apply Codex usage to AWS commits, and inherit Bedrock’s existing governance plane.

Why it matters: This is the tactical follow-through to signal #1, and the one you can act on this quarter. For AWS-standardized shops, you no longer need a separate OpenAI account or parallel governance to reach frontier OpenAI models. Codex on AWS is the bigger sleeper: engineering orgs that blocked Codex on procurement grounds now have a viable deployment path.

What to do: If you’re an AWS-first shop, get on the Bedrock GPT-5.5 waitlist this week and put one team on a pilot through Bedrock instead of the direct OpenAI API. Compare latency, governance overhead, and unit economics against Claude on Bedrock. That answer determines your model-routing architecture for 18 months or so.

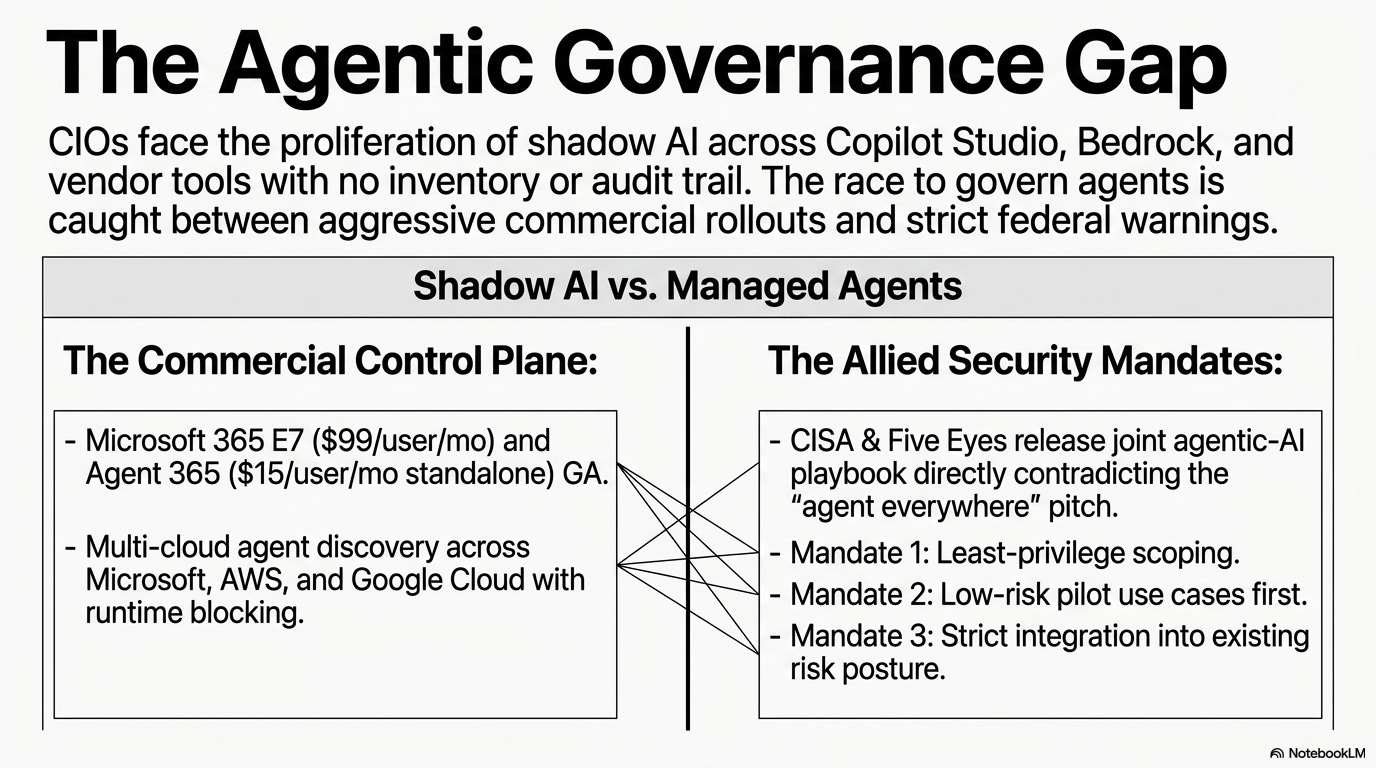

3. Microsoft 365 E7 and Agent 365 hit GA

What happened: On May 1, Microsoft made Microsoft 365 E7 ($99/user/month, the first major new M365 enterprise tier in over a decade) and Agent 365 ($15/user/month standalone) generally available. Agent 365 discovers agents (including shadow AI) across Microsoft, AWS Bedrock, and Google Cloud, applies policy through Entra, and hooks into Defender for runtime blocking. Asset context mapping and runtime blocking enter public preview in June.

Why it matters: Every CIO has the same problem: agents proliferating across Copilot Studio, Bedrock, Vertex, plus vendor agents from Salesforce, ServiceNow, and SAP, with no inventory, no policy plane, no audit trail. Microsoft is the first hyperscaler to ship a multi-cloud agent control plane priced as an enterprise SKU. Whether you adopt it or not, it just set the bar for “agent governance” in 2026.

What to do: Pull a list of agents running in your tenant: Copilot Studio, Power Platform, Azure AI Foundry, plus third-party agents touching M365. If you can’t produce that list in an hour, you have a governance problem regardless of vendor.

Don’t commit to E7 yet. Wait for the June previews and Google’s I/O response.

4. Pentagon signs seven AI vendors for classified networks — and freezes out Anthropic

What happened: On May 1, the Department of Defense announced agreements with 7 AI companies (SpaceX, OpenAI, Google, NVIDIA, Reflection AI, Microsoft, and AWS) to deploy on classified networks at Impact Level 6 and 7.

Anthropic was excluded after being designated a national security supply-chain risk in March (the first such designation against a US AI lab) for refusing unrestricted access to Claude for autonomous weapons and mass domestic surveillance.

Why it matters: 2 enterprise signals in one story. Frontier model selection is no longer purely a capability decision. For any company touching federal, defense, or critical infrastructure work, vendor political posture is now a procurement input. And Anthropic’s stance is the cleanest example yet of a frontier lab refusing a customer category on values grounds. The safety/ethics/usability tradeoff just got a price tag.

What to do: If you’re in financial services, healthcare, or any regulated sector with federal touchpoints, add “vendor government posture” to your AI vendor risk framework. If you’ve standardized on Claude for sensitive workloads, write down why before someone asks.

5. CISA and Five Eyes drop joint agentic-AI security playbook

What happened: On May 1, CISA, NSA, and Five Eyes partners (Australia, Canada, UK, New Zealand) released “Careful Adoption of Agentic AI Services”, the first joint allied guide specifically for agentic AI, not generic GenAI. The document calls out expanded attack surface, privilege creep, behavioral misalignment, and obscure event records as the core risks. Acting CISA Director Nick Andersen tied the release to the President’s Cyber Strategy for America. The PDF is hosted on media.defense.gov dated April 30.

Why it matters: Critical-infrastructure and defense customers will start citing this in RFPs and audit questionnaires within weeks. The three pillars CISA emphasized (least-privilege scoping, low-risk pilot use cases first, folding agents into existing risk posture) directly contradict the “agent everywhere, autonomously” pitch every enterprise vendor is planning this quarter. Five Eyes guidance also imports into UK, Australian, and Canadian procurement standards by reference, so this isn’t just a US signal.

What to do: Have your CISO map any production or in-flight agent deployment against the three CISA action items this week. Add the document to your AI governance reference set before Q2 audits. It will soon appear in your auditor’s question list whether you wait or not.

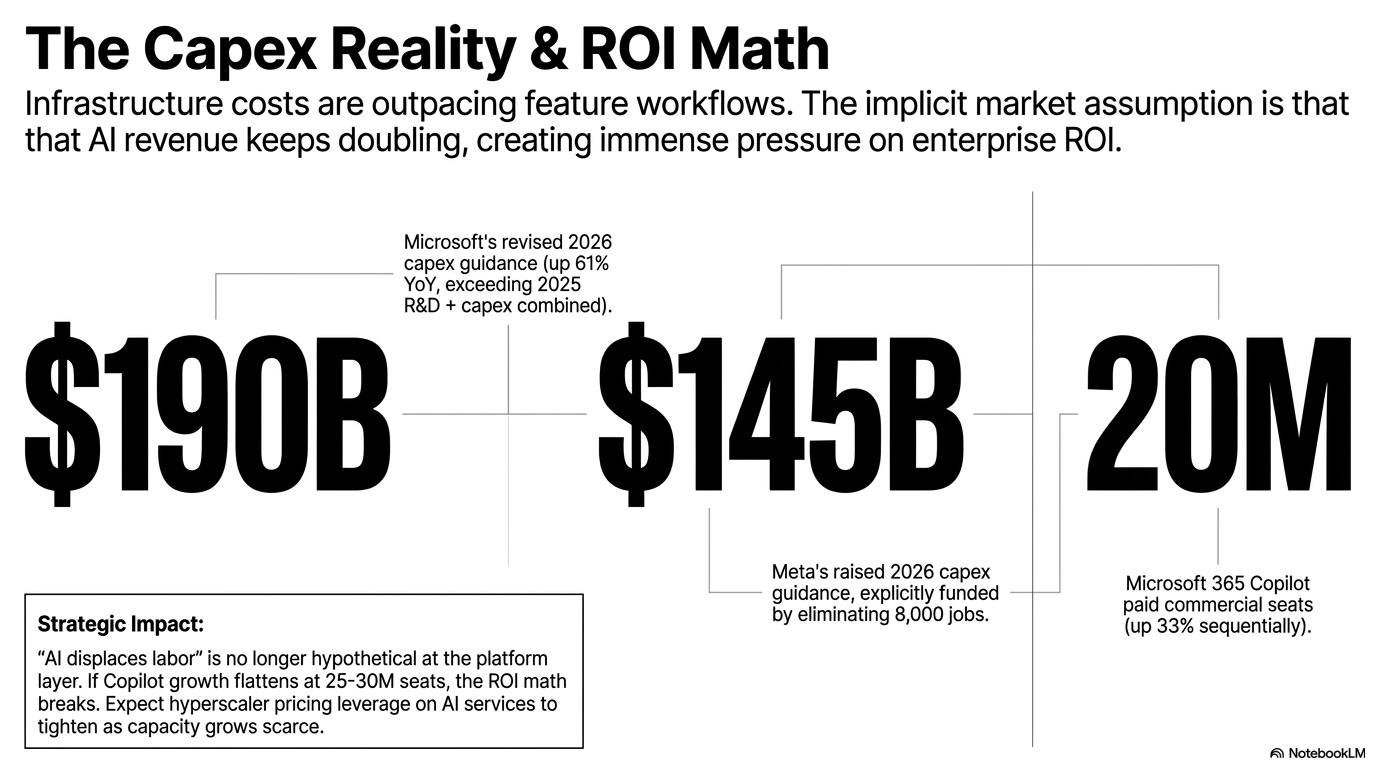

6. Microsoft Q3: Copilot crosses 20M paid seats, capex hits $190B

What happened: On April 29, Microsoft reported fiscal Q3 results. Revenue $82.9B, up 18%. Azure grew 40% (39% in constant currency). On the earnings call, Microsoft disclosed Microsoft 365 Copilot paid commercial seats crossed 20 million, up from 15M in January (roughly 33% growth in one quarter), total AI revenue annualized run rate hit $37 billion, up 123% YoY, and capex guidance for 2026 was raised to $190 billion, up 61% YoY.

Why it matters: Two competing signals in one note. Copilot adoption is compounding. 20M paid seats might signal the “feature in search of a workflow” critique night be over. The question shifted from “will Copilot stick” to “what should I displace with it.” Then there’s the capex curve: $190B is more than Microsoft’s entire 2025 R&D plus capex combined, and the implicit assumption is that AI revenue keeps doubling. If Copilot growth flattens at 25-30M seats, the ROI math gets brutal.

What to do: If your Copilot pilot is stuck below 30% adoption, the bottleneck is workflow design, not licenses. Run one targeted use case to over 70% before expanding seats. If you’re negotiating a 2026 EA renewal, capex pressure on Microsoft’s side gives you more leverage than at any point in the last five years.

7. Meta hikes 2026 capex to $145B, axes 8,000 jobs to pay for it

What happened: On April 29, Meta filed an 8-K reporting Q1 results of $56.3B revenue (+33% YoY) and raising its full-year 2026 capex guidance to $125-145B, up from $115-135B prior. The filing also disclosed a $107B step-up in contractual commitments tied to multi-year cloud and infrastructure deals. The next day, Zuckerberg told staff at an internal town hall that the 8,000 layoffs (announced April 24, starting May 20) are a direct consequence of compute spending: “We basically have two major cost centers: compute infrastructure and people-oriented things.”

Why it matters: Meta is the second hyperscaler this quarter, after Microsoft’s $190B, to publicly trade headcount for compute capacity. The 2026 capex guidance was raised mid-year, not at year-start, which means the AI infrastructure bill is outpacing forecasts even at the companies writing the checks. For CIOs, this signals hyperscaler pricing leverage on AI services is going up, not down. “AI displaces labor” is no longer hypothetical at the platform layer. Zuckerberg said it on the record.

What to do: Reprice your 2027 cloud and AI-compute budget assumptions this quarter. Assume hyperscaler list price holds and discounts shrink as capacity goes scarce. Pull forward any committed-spend negotiations with AWS, Azure, or GCP before contract renewals tighten.

8. EU AI Act trilogue collapses — high-risk deadline still legally August 2

What happened: In late April, the second political trilogue on the Digital Omnibus on AI ended without agreement. The Omnibus was the Commission’s November 2025 proposal to defer the AI Act’s high-risk obligations from August 2, 2026 to December 2, 2027. Without a deal before August 2, the original Act applies as written: full high-risk obligations kick in on schedule, and the harmonized standards meant to operationalize compliance aren’t ready.

Why it matters: For any US enterprise selling into the EU or running AI systems that touch EU users (employment, credit, health, critical infrastructure), the planning assumption flipped this week. Three months ago it looked safe to bet on the deferral. The legal default is now full applicability in 90 days. Betting on a deferral that hasn’t happened is a risky plan.

What to do: Get a Yes/No answer this week on whether any system you operate falls under Annex III high-risk categories: recruitment AI, credit scoring, biometric ID, critical infrastructure. If yes, you have until August 2 to be ready, even if the Omnibus eventually passes.

Brief your General Counsel; don’t wait for them to brief you.

What am I missing? If you operate EU AI Act-regulated systems and have an Annex III readiness plan that actually works, I’d like to hear it. Reply and tell me how you’re sequencing the next 90 days.

References:

Microsoft Official Blog — The next phase of the Microsoft-OpenAI partnership: https://blogs.microsoft.com/blog/2026/04/27/the-next-phase-of-the-microsoft-openai-partnership/

TechCrunch — OpenAI’s $50B AWS deal: https://techcrunch.com/2026/04/27/openai-ends-microsoft-legal-peril-over-its-50b-amazon-deal/

OpenAI — OpenAI models, Codex, and Managed Agents come to AWS: https://openai.com/index/openai-on-aws/

AWS Top Announcements: https://aws.amazon.com/blogs/aws/top-announcements-of-the-whats-next-with-aws-2026/

Microsoft Security Blog — Agent 365 GA: https://www.microsoft.com/en-us/security/blog/2026/05/01/microsoft-agent-365-now-generally-available-expands-capabilities-and-integrations/

Microsoft 365 E7 and Agent 365 GA: https://techcommunity.microsoft.com/blog/microsoft_365blog/microsoft-365-e7-and-agent-365-are-now-generally-available/4516295

DefenseNews — Pentagon freezes out Anthropic: https://www.defensenews.com/news/pentagon-congress/2026/05/01/pentagon-freezes-out-anthropic-as-it-signs-deals-with-ai-rivals/

OpenAI — Agreement with the Department of War: https://openai.com/index/our-agreement-with-the-department-of-war/

CISA — US and international partners release guide to secure adoption of agentic AI: https://www.cisa.gov/news-events/news/cisa-us-and-international-partners-release-guide-secure-adoption-agentic-ai

DoD media — Careful Adoption of Agentic AI Services (PDF): https://media.defense.gov/2026/Apr/30/2003922823/-1/-1/0/CAREFUL%20ADOPTION%20OF%20AGENTIC%20AI%20SERVICES_FINAL.PDF

Microsoft Source — Q3 FY26 results: https://news.microsoft.com/source/2026/04/29/microsoft-cloud-and-ai-strength-fuels-third-quarter-results/

Microsoft Investor Relations FY26 Q3: https://www.microsoft.com/en-us/investor/earnings/fy-2026-q3/press-release-webcast

Meta SEC EDGAR 8-K filings: https://www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=0001326801&type=8-K&dateb=&owner=include&count=40

EU Digital Strategy — Navigating the AI Act FAQ: https://digital-strategy.ec.europa.eu/en/faqs/navigating-ai-act

DLA Piper — Digital AI Omnibus analysis: https://knowledge.dlapiper.com/dlapiperknowledge/globalemploymentlatestdevelopments/2026/The-Digital-AI-Omnibus-Proposed-deferral-of-high-risk-AI-obligations-under-the-AI-Act