AI Waypoints: Week of June 1, 2026 — Edition #12

The week enterprise AI's numbers got real — Anthropic $965B valuation, Dell's $51.3B AI server backlog, Salesforce books 28.6T tokens

Good morning. This was the week the enterprise AI conversation stopped trafficking in forecasts and started reading earnings reports. Anthropic raised $65 billion at a $965 billion valuation. Dell printed a $51.3 billion AI server backlog. Salesforce disclosed 28.6 trillion tokens processed last quarter. As it’s becoming a regular occurrence, 2 of the 7 signals below are Anthropic; the financing and the Opus 4.8 release landed on the same day.

1. Anthropic raised $65B at a $965B valuation — and disclosed $47B run-rate revenue

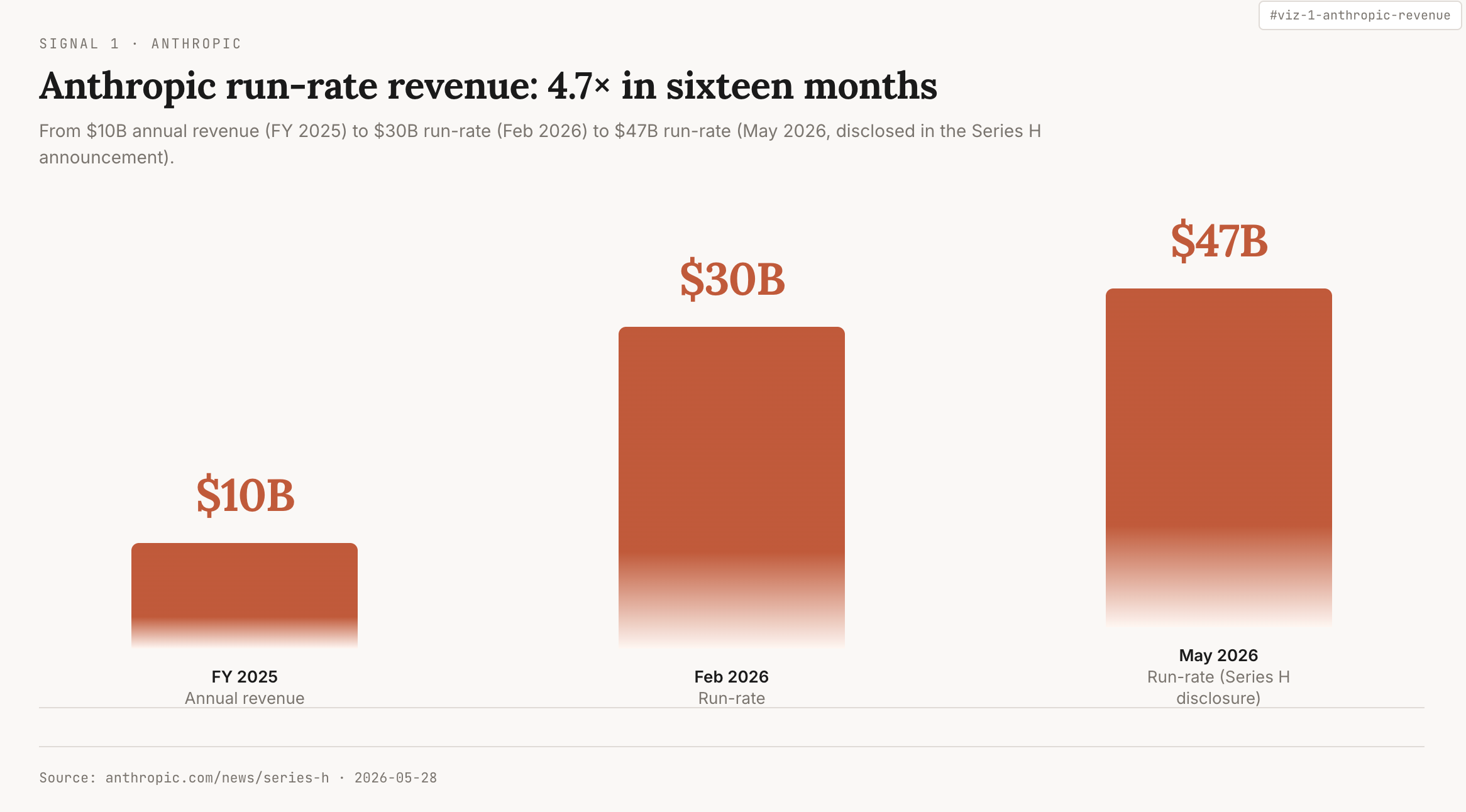

What happened: Anthropic closed a $65 billion Series H on May 28 at a $965 billion post-money valuation, the largest private financing round on record. Lead investors: Altimeter, Dragoneer, Greenoaks, Sequoia. Co-leads: Capital Group, Coatue, D1, GIC, ICONIQ, XN. The filing tucks in a number Anthropic had not published before: “run-rate revenue crossed $47 billion earlier this month,” up from $30B in February and $10B in annual revenue last year. Samsung, SK hynix, and Micron Technology were named “strategic infrastructure partners.” That’s the first explicit memory-supply link I’ve seen called out in a frontier-lab financing.

Total disclosed compute commitments now sit at Amazon (~5 gigawatts), Google/Broadcom (~5GW of Tensor Processing Unit capacity), and SpaceX/xAI Colossus 1 access through May 2029 ($40B+ per the xAI S-1).

Why it matters: The $965B valuation tops OpenAI’s most recent private mark, and the $47B run-rate is the first solidly sourced number any of us can use to size our own Anthropic spend against the supplier. The memory-supply line is the part that changes the vendor-risk conversation. Vendor-risk teams have been asking quietly for a year what happens if NVIDIA allocation slips for the model lab they already standardized on, and “partner of record with Samsung, SK hynix, and Micron” is the kind of answer they did not have last quarter. For regulated buyers, the concentration question has shifted from “is this vendor big enough to absorb our usage” to “is this vendor so central to the whole compute supply chain that switching costs are now structural.”

ELI5: What’s the memory-supply story, and why does it move the vendor-risk needle?

AI models need a specific high-end chip called high-bandwidth memory, and it has been in short supply for two years. Samsung, SK hynix, and Micron make almost all of it. Anthropic just got named “strategic infrastructure partner” by all three, which is the supply-chain version of a restaurant becoming the preferred buyer at the three biggest produce farms in the country. Good news if Claude is already in your stack; trickier later if you decide to switch labs, because the next one may not have the same kind of supply guarantee behind it.

What to do: If Claude is in your inference stack, I’d get the Series H disclosure into your next vendor-risk packet before renewal. Ask your CFO whether your contracted Anthropic spend as a share of disclosed run-rate exceeds your own internal vendor-concentration threshold, and whether the multi-cloud compute footprint (Amazon Web Services, Google Cloud, xAI Colossus) changes your data-residency model in the US and outside.

2. Claude Opus 4.8 shipped the same day — Fast mode at $10/$50 and “hundreds of parallel subagents”

What happened: Anthropic also released Claude Opus 4.8 on May 28, an unusual product-plus-capital double announcement.

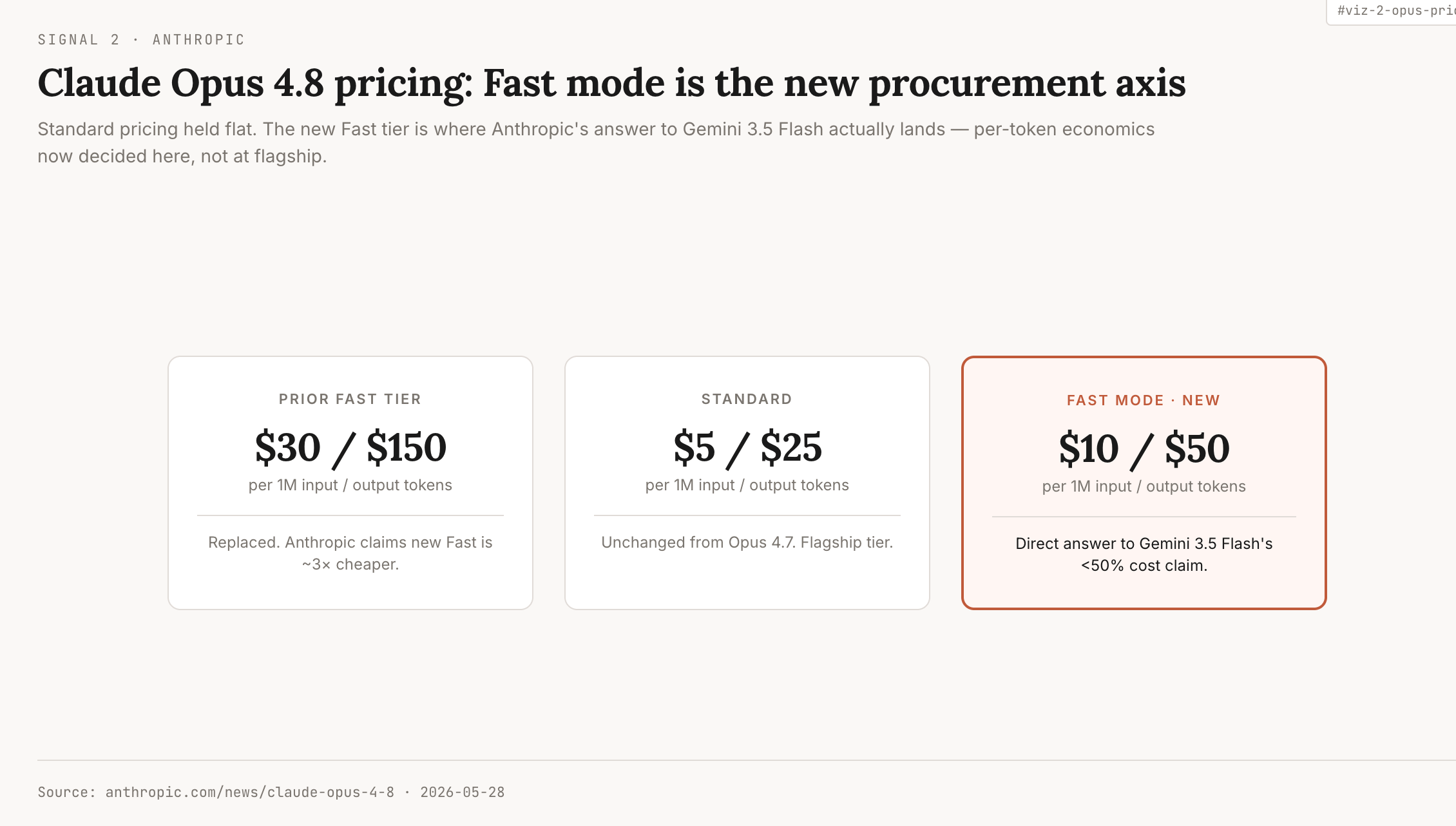

Standard pricing held at $5 input and $25 output per million tokens.

A new Fast mode sits at $10 input and $50 output per million

Anthropic claims it is roughly 3x cheaper than the prior fast tier.

Benchmarks:

Online-Mind2Web at 84%;

the Legal Agent Benchmark all-pass standard crossed for the first time at >10%;

about 4x less likely to overlook code flaws than Opus 4.7.

Two new capabilities: Effort Control (per-turn effort selection in claude.ai and Claude Cowork), and a Dynamic Workflows research preview in Claude Code that Anthropic describes as supporting “hundreds of parallel subagents“ for large-scale code migrations. The Messages application programming interface (API) now accepts mid-conversation system entries without breaking prompt caching.

Why it matters: Three threads here, not one. The Fast mode price point ($10/$50) is Anthropic’s direct answer to Gemini 3.5 Flash’s <50% cost claim from Edition #11. Per-token economics for Claude versus Gemini are now decided at the Fast/Flash tier, not at flagship, which is a meaningfully different procurement conversation than the one I was having in April.

“Hundreds of parallel subagents” is the first concrete capability reason to spend the new metered credits from the June 15 cutover I covered last week; large-codebase migrations could move from weeks-per-repo toward hours-per-repo if the parallelism holds true. The Legal Agent Benchmark breakthrough lands one week before the PwC, KPMG, and Deloitte alliances start serving tax and legal clients on Claude. That is now the product behind the consulting alliance.

ELI5: What’s the Legal Agent Benchmark, and why is “all-pass” the line that mattered?

Think of the Legal Agent Benchmark as the SAT for AI doing legal work: a standardized test suite that grades models on real lawyering tasks like contract review, statute interpretation, and due-diligence drafts. The “all-pass” bar means a model has to get every question right at the toughest grading level, not just clear the average. No model had cleared that bar before; Opus 4.8 is the first. That matters right now because PwC, KPMG, and Deloitte just told their tax and legal clients they are running on Claude — they need a model that can defend its answer to a partner, not just sound plausible to a junior associate.

What to do: If you’re running Claude Code for production work, side-by-side Opus 4.8 standard against Opus 4.8 Fast on your hardest 50-file migration this week. If Fast delivers comparable quality at 60% lower cost, the June 15 metered cutover gets cheaper to live with. Before signing any tax or legal services contract with a Big-4 partner, ask which model version they will hold for the engagement. Model swaps mid-engagement create new audit-evidence chains.

3. Salesforce Agentforce hit $1.2B annual recurring revenue — and named a 1.5x customer-spend lift

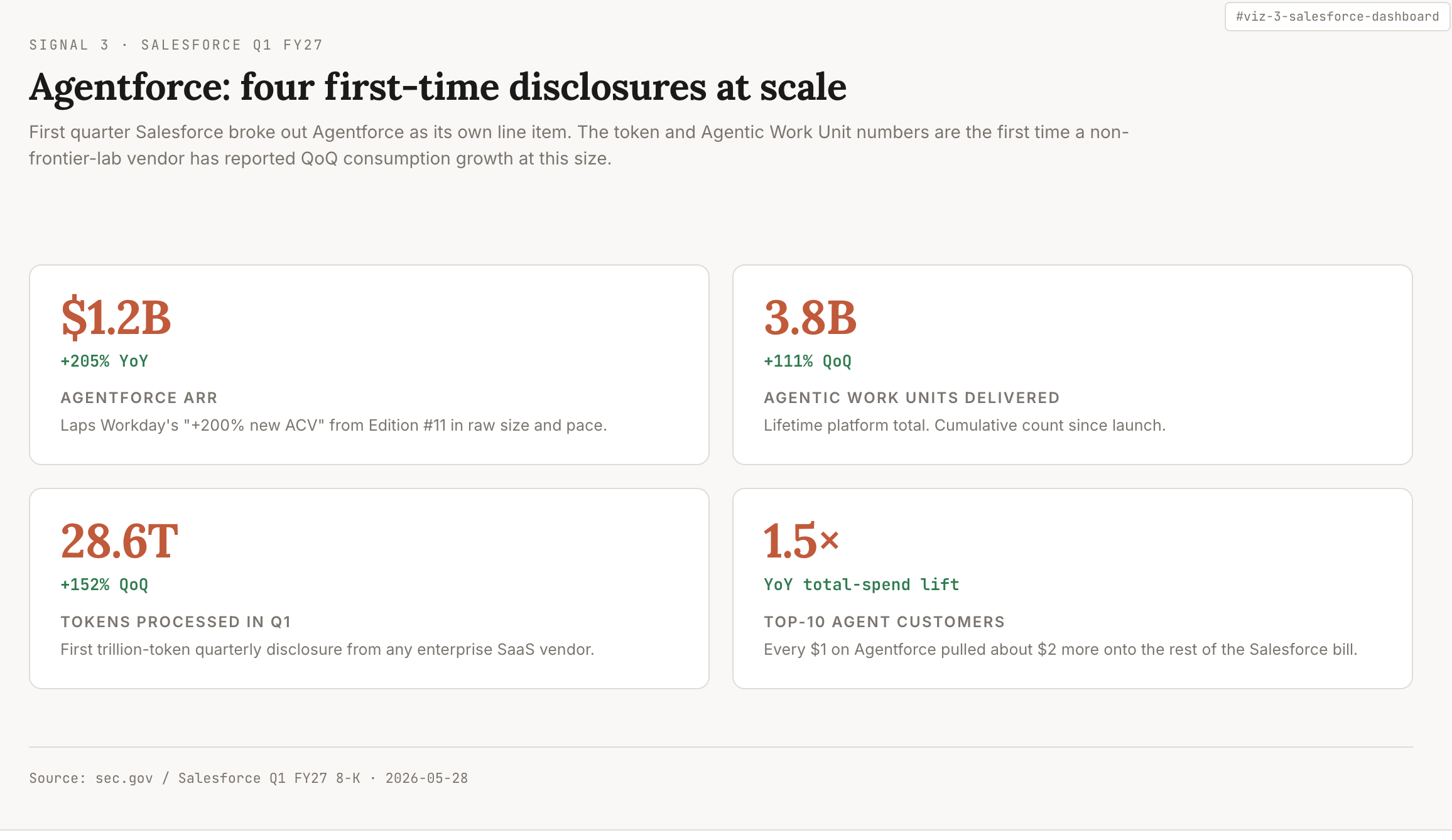

What happened: Salesforce reported Q1 FY27 on May 28: total revenue $11.13B (+13% year-over-year), beating $11.05B consensus. Agentforce plus Data 360 annual recurring revenue (ARR) is nearly $3.4B (+>200% YoY), broken out as $1.2B Agentforce ARR (+205% YoY) and $1.1B Informatica Cloud ARR after the acquisition closed ahead of schedule.

First-time operational disclosures at this scale:

3.8 billion Agentic Work Units delivered to date (+111% quarter-over-quarter);

28.6 trillion tokens processed (+152% QoQ);

98 deals greater than $1M annual contract value in Q1, a Q1 record per CEO Marc Benioff.

Top-10 customers by agent usage increased total Salesforce spend 1.5x year-over-year, per Chief Revenue Officer Miguel Milano. Capital return: $27.5B year-to-date including a new $25B accelerated buyback.

FY27 revenue guide raised to $45.9-46.2B.

Why it matters: $1.2B Agentforce ARR at +205% is now the largest hard-number proof point in the enterprise-AI agent race; it laps Workday’s “+200% new annual contract value” from Edition #11 in raw size and pace. The 28.6T-token disclosure (+152% QoQ) is the cleaner second read. It is the first time a non-frontier-lab vendor has published quarter-over-quarter token-consumption growth at this scale, which means a buyer can finally hold their own Agentforce growth up against the platform-wide pace and see whether they are an outlier on either side. The 1.5x customer-spend lift among top-10 agent users is the cleanest revenue-uplift number any agent vendor has published. Every $1 a customer spends on Agentforce pulls about $2 more onto the rest of their Salesforce bill.

What to do: If you’re in a Salesforce renewal in H2 2026, ask for your tenant’s Agentic Work Unit consumption against the 3.8B platform baseline, and have procurement model the 1.5x spend-lift scenario as a hard ceiling, not a forecast. If Agentforce is on your platform and your CFO has not seen tenant-level usage data, get it on the next quarterly business review (QBR). The vendor-side 28.6T number is only useful to you if it can be broken down to your seat count.

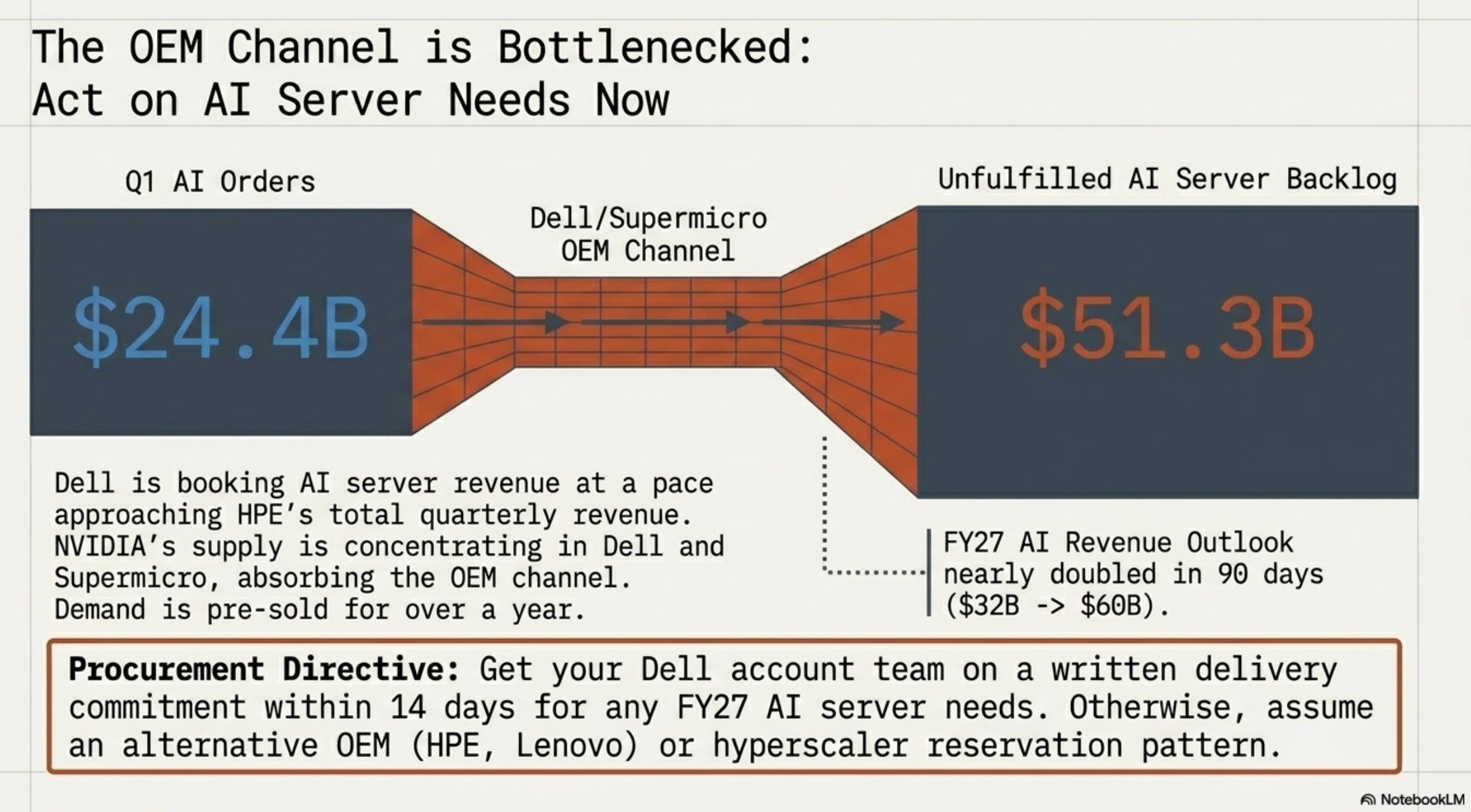

4. Dell’s AI server backlog hit $51.3B — and the FY27 outlook nearly doubled in 90 days

What happened: Dell Technologies reported Q1 FY27 on May 28: total revenue $43.8B (+88% YoY, a record). AI-Optimized Servers revenue $16.1B (+757% YoY, also a record). AI server orders booked in Q1: $24.4B. AI server backlog at quarter-end: $51.3B. Non-GAAP earnings per share $4.86 versus $2.94 consensus. FY27 outlook raised to $167B total revenue and $60B AI server revenue, up from a prior $32B AI server target only 90 days ago. Stock closed +32% on May 29, Dell’s best single-day gain on record.

Why it matters: $24.4B in Q1 AI orders against a $51.3B backlog means Dell has more than a year of demand pre-sold. The original equipment manufacturer (OEM) channel for enterprise AI infrastructure is supply-constrained, not demand-constrained. The AI revenue outlook nearly doubled ($32B to $60B) in 90 days, which is the OEM-level confirmation that NVIDIA’s Q1 FY27 $91B Q2 guide from Edition #11 is concentrating in Dell and Supermicro rather than getting redistributed across channels.

With $16.1B AI server revenue in a single quarter, Dell is now booking AI server revenue at a pace that approaches Hewlett Packard Enterprise’s total quarterly revenue (~$9.6-10B expected Q2). Dell and Supermicro are absorbing the OEM channel, and most enterprise AI infrastructure procurement running today is downstream of that.

What to do: Get your Dell account team on a written delivery commitment within 14 days for any AI server need in FY27. The backlog math says new orders entering today are unlikely to ship inside fiscal year-end unless you are already in the queue. If you are not, your H2 2026 AI infrastructure plan should assume an alternative OEM (Supermicro, Hewlett Packard Enterprise, Lenovo) or a hyperscaler reservation pattern, not a Dell on-prem build.

5. Snowflake committed $6B to AWS over five years — and named Graviton, not GPUs

What happened: Snowflake reported Q1 FY27 on May 28: revenue $1.39B (+33% YoY); product revenue $1.33B (+34% YoY); net revenue retention 126%; 779 customers with trailing-12-month product revenue greater than $1M (+29% YoY); remaining performance obligation $9.21B (+38% YoY). Stock +39% intraday on May 28.

The same week, Snowflake announced a multi-year strategic collaboration agreement with Amazon Web Services: a $6 billion commitment over five years, named as the largest infrastructure commitment to date in the company’s relationship with AWS. The compute layer is named explicitly: Amazon Web Services Graviton plus AI capacity for agentic workloads.

Why it matters: The $6B commitment is the most informative number in the enterprise data layer this quarter, and I had to read the release twice to fully see why. Snowflake’s gross compute spend is now growing roughly 5x its IPO baseline despite the historical “data warehouse” label. In a way, they are an AI compute reseller wearing a database title.

AWS Graviton (Arm-based central processing unit), not NVIDIA Graphics Processing Units, is named as the compute layer, which is the strongest signal yet that Arm-based inference is moving from hyperscaler-internal to independent software vendor commercial. The five-year horizon brackets the same compute window as Anthropic’s xAI Colossus deal in Signal 1, and both labs are now spoken-for through 2029.

What to do: If Snowflake is your data platform, ask your account team this week which workloads are moving to Graviton and what the per-credit price implication is. If Graviton-priced credits are cheaper, the five-year commitment is being passed through to you, so make sure you are at the right tier.

If your 2027 AI infrastructure plan assumes NVIDIA-only inference, the Snowflake-plus-Graviton commitment is a directional signal that the Arm inference path is well-funded enough to model as a serious second source.

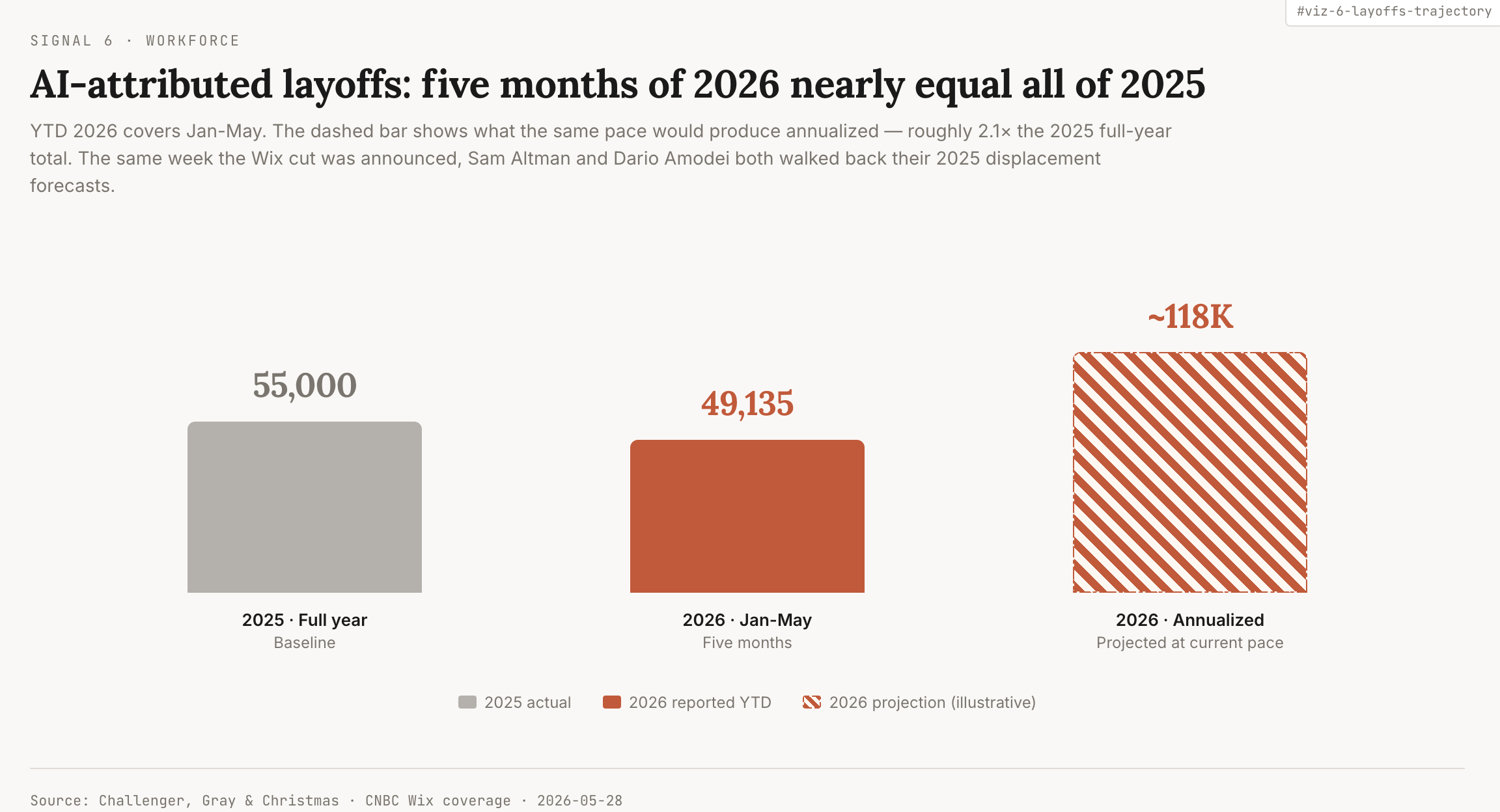

6. Wix cut 1,000 jobs — and three high-profile CEOs walked back AI-displacement messaging the same week

What happened: Wix CEO Avishai Abrahami announced on May 28 that the website-builder will cut about 1,000 employees, roughly 20% of its 5,277-person workforce. Stated drivers: “fast evolution of AI capabilities“ and the strengthened Israeli shekel. Abrahami’s framing: “We have witnessed the most significant shift in how companies are built since the invention of modern programming languages in the 1970s.“

Year-to-date 2026 tech layoffs total roughly 115,430 across 152 companies, versus 124,636 across 275 companies in all of 2025, per outplacement firm Challenger, Gray & Christmas. AI-attributed layoffs year-to-date: 49,135, close to the full-year 2025 total of 55,000 with seven months still to run.

Three counter-frames landed inside six days.

On May 26, OpenAI CEO Sam Altman told a Commonwealth Bank of Australia audience he had been “pretty wrong“ on AI’s economic impact, and added, “I thought there would have been more impact on entry-level white-collar jobs being eliminated by now than has actually happened.” That’s a direct walk-back of his own June 2025 warning (Fortune, May 26).

The same Fortune piece reports Anthropic CEO Dario Amodei walking back similar earlier framing the same week, with both reversals landing ahead of expected IPOs.

The third voice came one day later, May 27, from Box CEO Aaron Levie, who called the trend “AI psychosis“ and argued chief executives are “sufficiently distant from the last mile of work“ to misread agent capability.

Why it matters: The Wix announcement crossed the threshold where five months of AI-attributed layoffs (49,135) nearly equal the full 2025 total (55,000). Pair this with Standard Chartered’s 7,800 commitment to 2030 from Edition #11, and the picture lands on both sides at once. Real headcount cuts are getting announced, while the three highest-profile voices in the field (two frontier-lab CEOs and one enterprise software CEO) are naming the broader displacement story as ahead of confirmed execution.

I’m still working out where the truth between those two pictures lands, and that is the actual signal. Altman’s “delighted to be wrong“ reversal is the strongest of the three because he made the original prediction himself in June 2025, and Amodei’s reversal in the same Fortune piece mirrors it. Both land inside the same six days as Wix’s named cut.

The board question for enterprise architects has shifted from “will we be asked for an AI-displacement target” to “is the target arriving on the table built on confirmed productivity, or on the same forecast curve the model labs just started walking back.”

What to do: Before your next workforce-planning cycle, decide who in the architecture function owns the “what AI actually displaces” model, and run it before HR runs theirs.

A defensible per-process automation savings model needs to distinguish

confirmed productivity in production,

plausible 12-month productivity,

speculative 24-month productivity.

Without that breakdown, your headcount conversation is a number, not a plan.

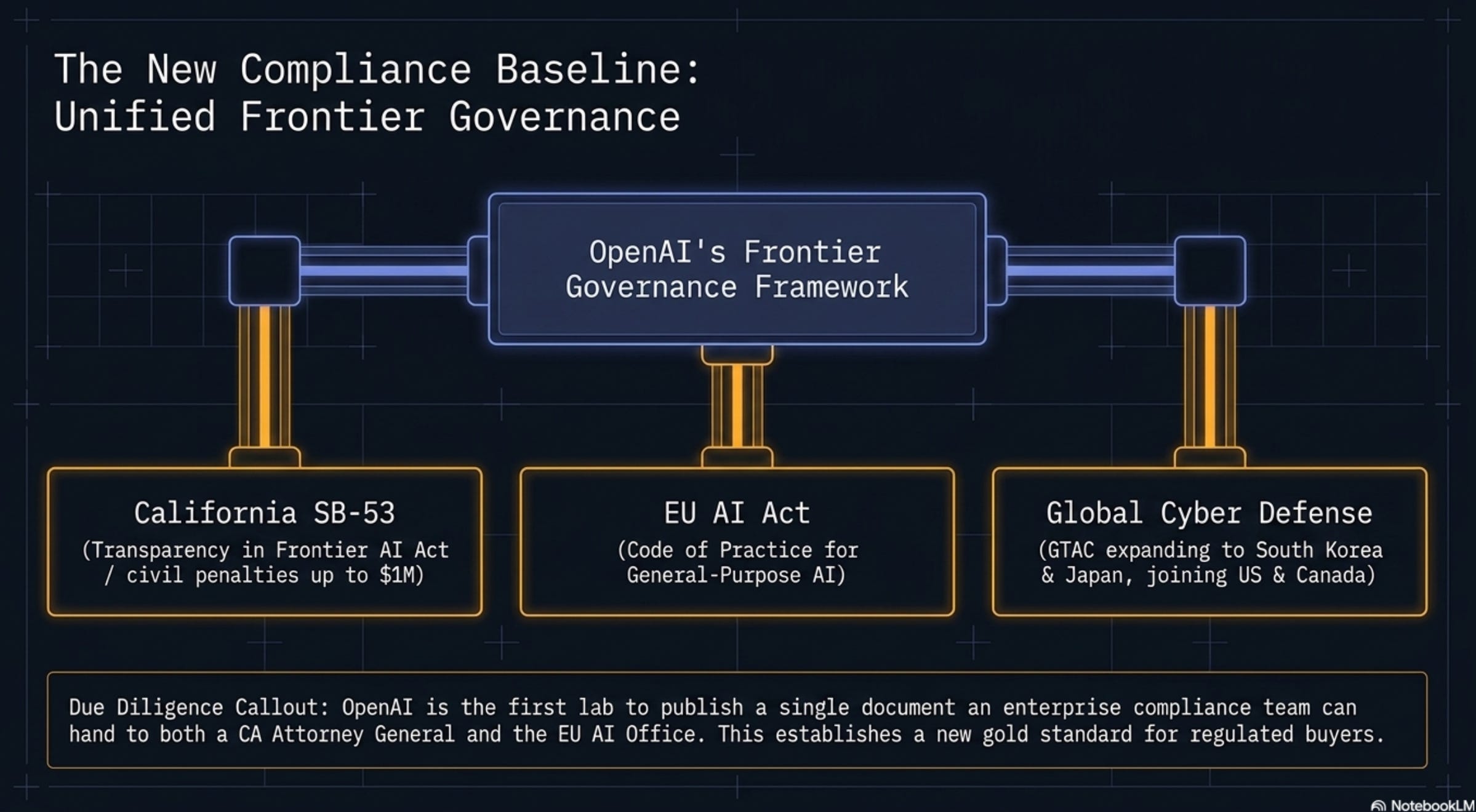

7. OpenAI’s Frontier Governance Framework maps to SB-53 plus the EU AI Act — and South Korea joined GTAC

What happened: OpenAI published its Frontier Governance Framework on May 29, the first frontier-lab governance document that explicitly maps its safety practices to

California’s Transparency in Frontier Artificial Intelligence Act (Senate Bill 53, in force since January 1, 2026)

the European Union AI Act Code of Practice for General-Purpose AI.

Coverage areas:

risk assessment across cyber-offense,

chemical/biological/radiological/nuclear (CBRN),

harmful manipulation, and

loss-of-control risks;

model reporting;

security risk management;

incident response;

external expert input;

update cadence.

Companion announcement the same week: the Government Trusted Access for Cyber program (GTAC) expanded to South Korea and Japan. Korea is now the third country globally (after the United States and Canada) to formally accede. About 130 Korean enterprise executives attended a Seoul exec summit on May 29. OpenAI also retired o3 and GPT-4.5 with sunset dates and added Computer Use on Windows for ChatGPT Enterprise and Codex.

Why it matters: OpenAI is the first frontier lab to publish a single document an enterprise compliance team can hand to

a California Attorney General responding to SB-53 enforcement (civil penalties up to $1 million per violation), and

the European Union AI Office responding to the General-Purpose AI Code of Practice.

That changes vendor due-diligence packets for every regulated buyer. Anthropic, Google DeepMind, and Meta will be asked for equivalent dual-mapped documents within 30 days.

The Korea and Japan GTAC accession is the first concrete sign I’ve seen that allied-government cyber-defense access is becoming a standard frontier-lab feature rather than a one-off, and it lines up against Anthropic’s Project Glasswing from Edition #11 on the security side.

What to do: Add OpenAI’s Frontier Governance Framework to your enterprise AI vendor due-diligence checklist this week. Then issue the same request to Anthropic, Google DeepMind, Meta, and Microsoft Research: a single document mapping your frontier safety practices to SB-53 plus the EU AI Act General-Purpose AI Code of Practice. Track whether they produce one in 60 days.

If you operate in South Korea, Japan, or Canada, ask whether GTAC (or Anthropic’s Project Glasswing partner program) is in scope for your regional Chief Information Security Officer (CISO) conversations.

What am I missing? Microsoft Build 2026 lands June 2-3 with expected Azure AI Foundry updates and a homegrown coding model; that is Edition #13. CrowdStrike Q1 FY27 prints June 3. Jensen Huang’s GPU Technology Conference (GTC) Taipei keynote is June 1 Taipei time. If you saw something in window I should have led with, reply and tell me. I’m also curious whether anyone has run Opus 4.8 Fast against Gemini 3.5 Flash side-by-side on a real production workload yet. I’d like to see the numbers.

References:

Anthropic Series H announcement (Anthropic Newsroom, 2026-05-28): https://www.anthropic.com/news/series-h

Claude Opus 4.8 (Anthropic Newsroom, 2026-05-28): https://www.anthropic.com/news/claude-opus-4-8

Salesforce Q1 FY27 Form 8-K (SEC EDGAR, 2026-05-28): https://www.sec.gov/Archives/edgar/data/0001108524/000110852426000125/crm-q1fy27xexhibit991.htm

Dell Technologies Q1 FY27 Form 8-K (SEC EDGAR, 2026-05-28): https://www.sec.gov/Archives/edgar/data/0001571996/000157199626000021/exhibit991earnings8kq1fy27.htm

Snowflake Expands AWS Collaboration with $6B Commitment (Snowflake Newsroom, 2026-05-27): https://www.snowflake.com/en/news/press-releases/snowflake-expands-aws-collaboration-with-6b-commitment-to-accelerate-enterprise-agentic-ai-adoption/

AI part of another tech layoff as Wix CEO announces 20% workforce cut (CNBC, 2026-05-28): https://www.cnbc.com/2026/05/28/wix-layoffs-ai-exchange-rates.html

Sam Altman and Dario Amodei are both walking back their AI jobs apocalypse prophecies as they eye blockbuster IPOs (Fortune, 2026-05-26): https://fortune.com/2026/05/26/sam-altman-dario-amodei-walking-back-ai-jobs-apocalypse-prophecies-ipo/

OpenAI’s Frontier Governance Framework (OpenAI Index, 2026-05-29): https://openai.com/index/openai-frontier-governance-framework/