AI Waypoints: Week of April 20, 2026 — Edition #6

Good morning. The bundling wars went vertical this week. ServiceNow is flattening its AI pricing, Microsoft’s E7 is absorbing the agent layer, and Novo Nordisk just handed Workday its largest AI implementation contract. Meanwhile, the compute arms race passed a threshold that makes the cloud buildout of the 2010s look like a rounding error.

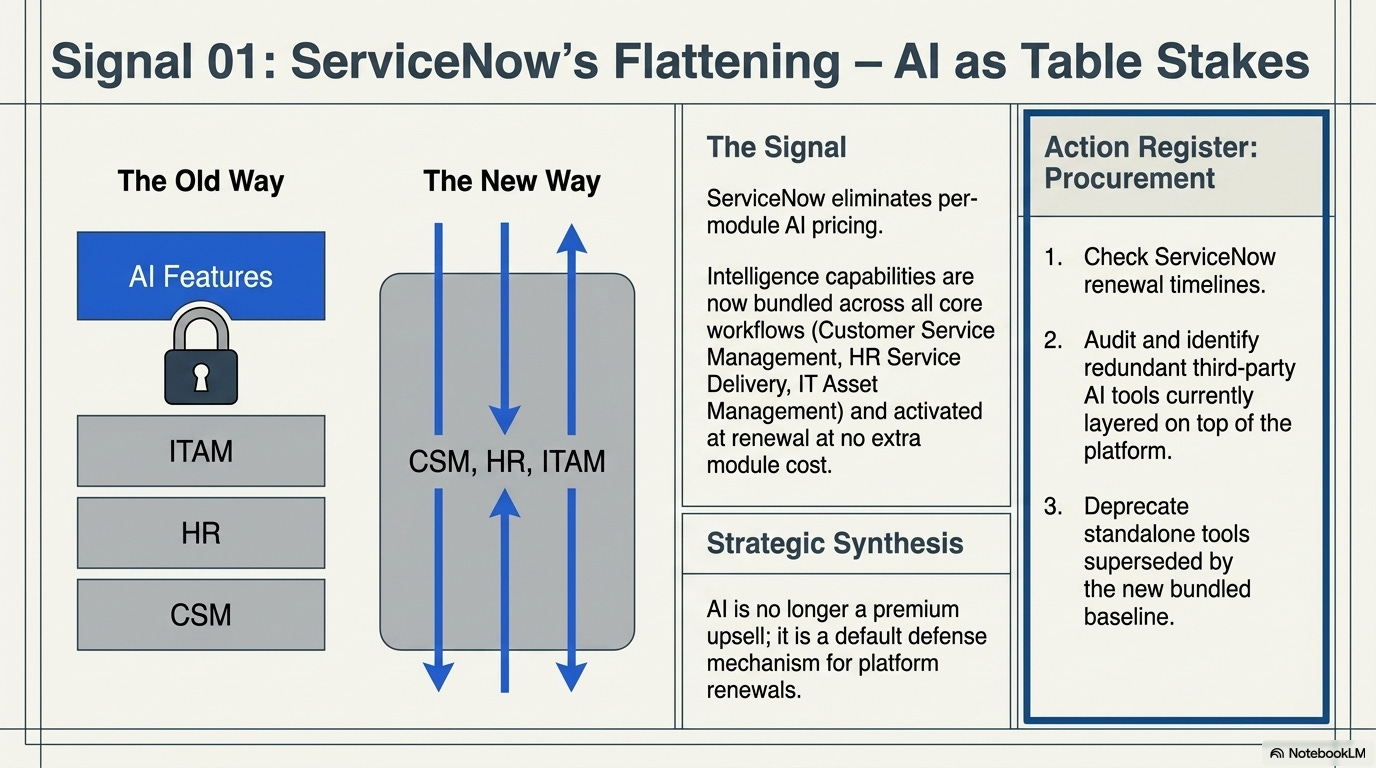

1. ServiceNow eliminates per-module AI pricing — bundles intelligence across all product tiers

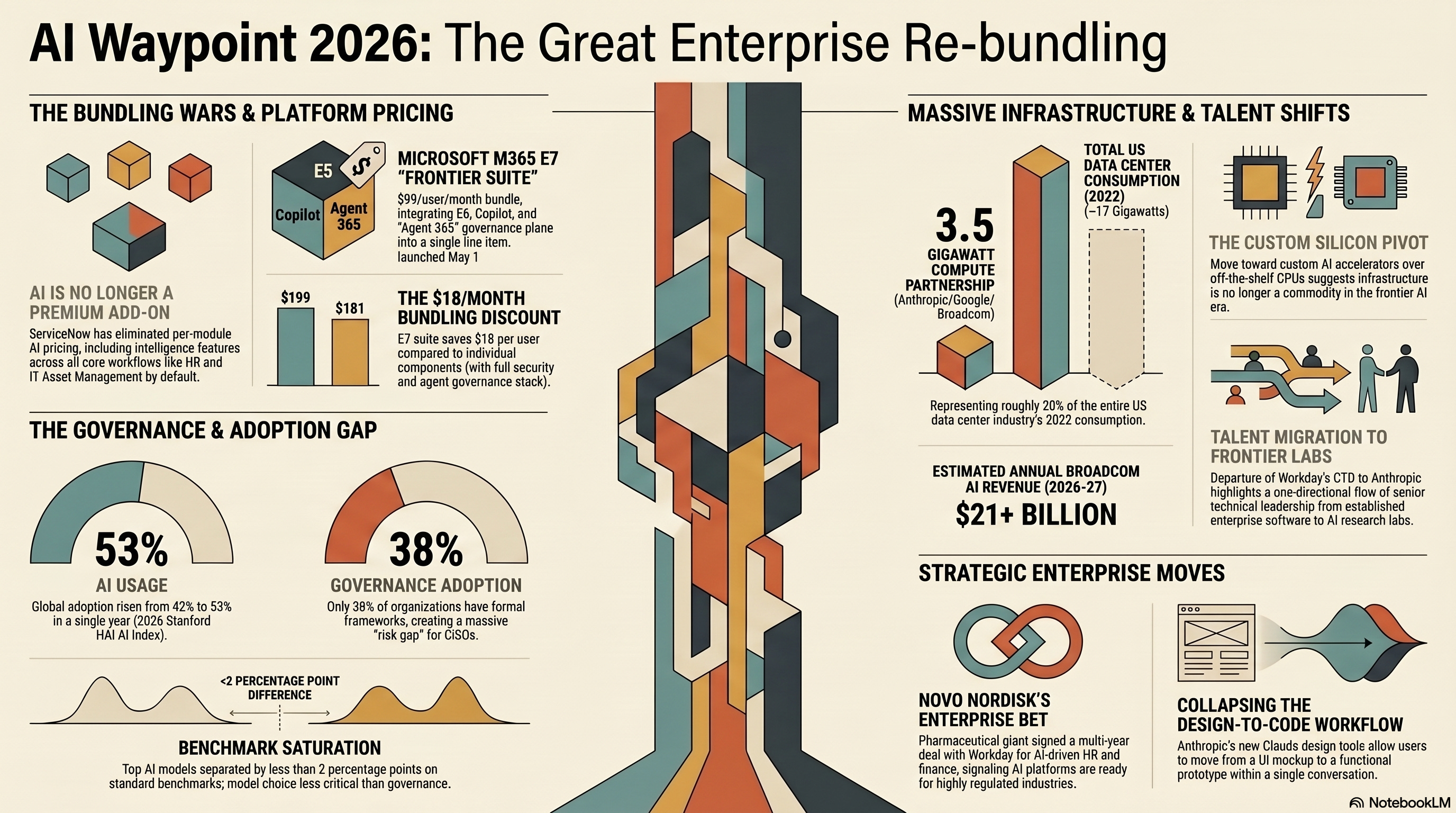

What happened: ServiceNow announced it will include AI capabilities across all product tiers, eliminating the separate per-module pricing that previously gated access to its intelligence features. The change applies to Customer Service Management, HR Service Delivery, IT Asset Management, and other core workflows. Existing customers on active contracts will see the AI capabilities activated at renewal without additional per-module fees.

Why it matters: This is the clearest signal yet that AI is becoming table stakes in enterprise platform pricing, not a premium add-on. ServiceNow joins SAP (bundling Business AI into two-thirds of cloud deals, as I covered in Edition #5) in treating AI as a default capability rather than an upsell. The competitive pressure is obvious: if your ITSM or HR platform charges extra for AI, your renewal conversation just got harder. For procurement teams, the interesting question is whether “included” means the capability is genuinely production-ready or whether it creates a new consulting and configuration revenue stream that replaces the module fee.

What to do: If you run ServiceNow, check your renewal timeline and ask your account team what the bundled AI capabilities include at your current tier. Compare the included functionality against any third-party AI tools you’ve layered on top. The bundling may make some of those redundant.

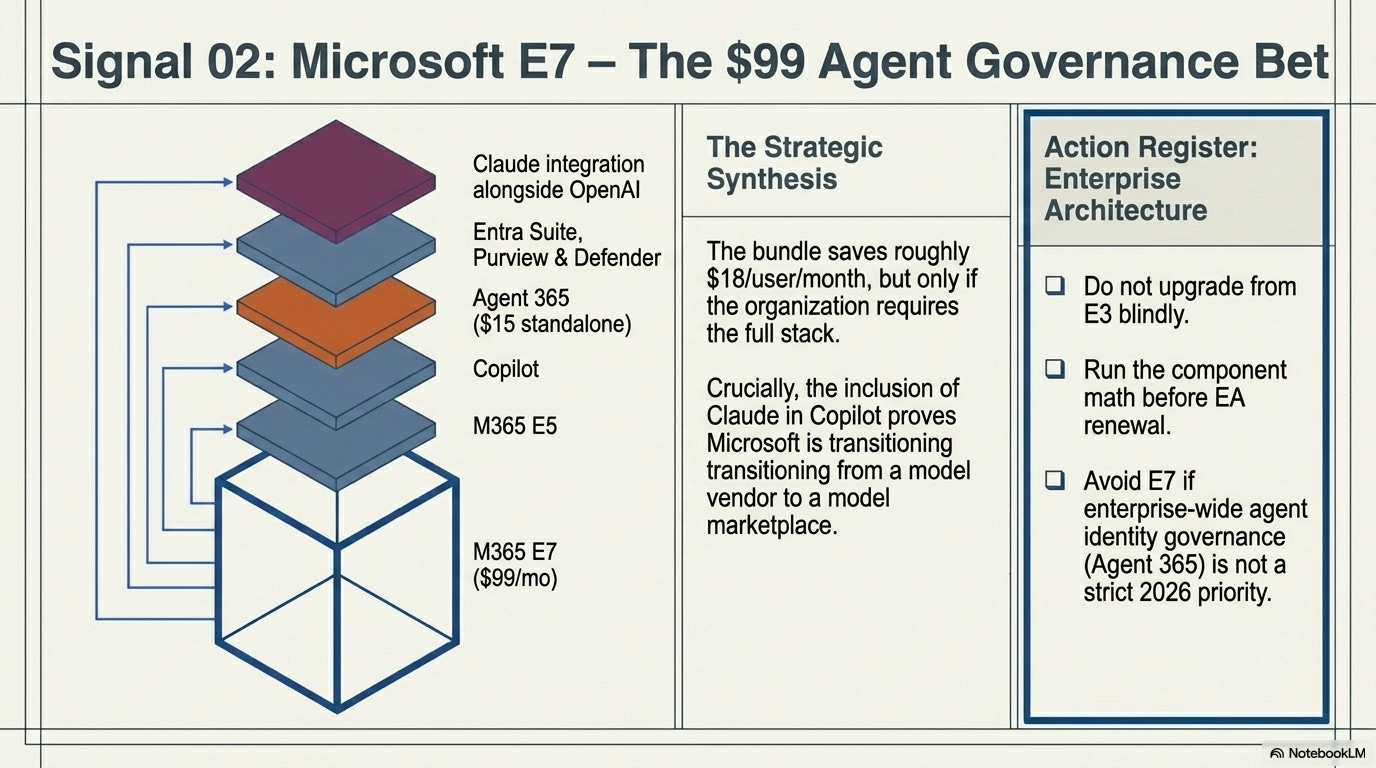

2. Microsoft E7 goes live — the $99/seat bet on agent governance

What happened: Microsoft 365 E7 “Frontier Suite” became transactable on May 1 at $99/user/month. The bundle includes E5 as the base, Microsoft 365 Copilot (the enterprise AI assistant), Agent 365 (the agent governance control plane at $15/user/month standalone), and the Entra Suite for identity, plus advanced Defender, Purview, and Intune capabilities. Claude is available alongside OpenAI models in Copilot chat via the Frontier program.

Why it matters: E7 is the first hyperscaler bundle that packages AI productivity, agent governance, and security into a single line item. The $99 price point saves roughly $18/user/month versus buying the components separately — but only if your organization actually needs the full stack (Agent 365, Purview, Defender, Copilot). As I noted when E7 was announced in Edition #4, the savings are conditional. Organizations not committing to agent identity governance across the Microsoft ecosystem should buy components separately rather than locking into the full bundle. The inclusion of Claude in Copilot alongside OpenAI models is the more significant long-term signal: Microsoft is becoming a model marketplace, not a model vendor.

What to do: Run the math on your current Microsoft licensing stack before your next EA renewal. If you’re already paying for E5, Copilot, and security add-ons separately, E7 may save money. If you’re on E3 and don’t need the full Purview/Defender/Agent 365 stack, upgrading to E7 is overpaying for capabilities you won’t use this year.

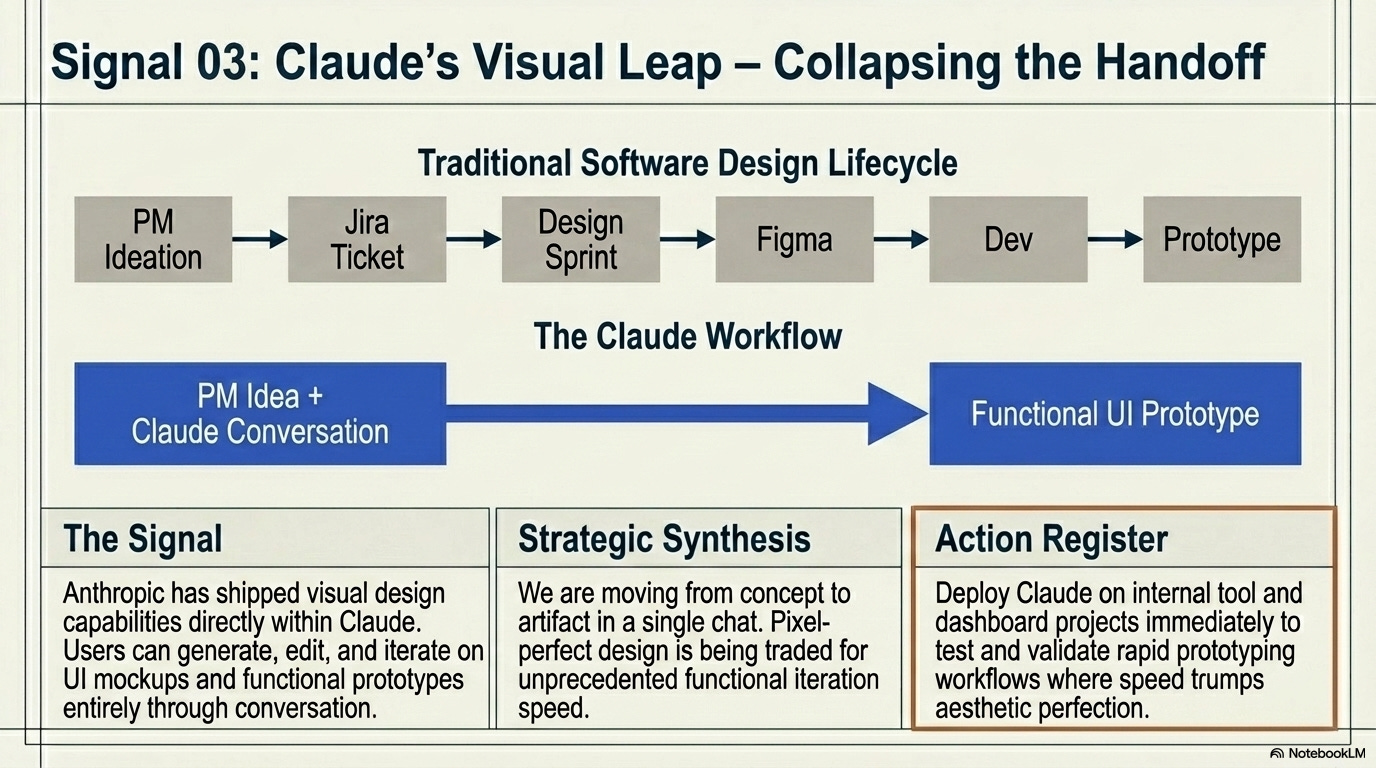

3. Anthropic ships Claude design tools — AI moves from text to visual creation

What happened: Anthropic Labs shipped a suite of visual design capabilities in Claude, enabling users to create, edit, and iterate on UI mockups, diagrams, and visual assets directly in conversation. The tools integrate with Claude’s existing coding and analysis capabilities, allowing users to move from concept to functional prototype without switching to separate design software.

Why it matters: This isn’t about competing with Figma. It’s about collapsing the distance between idea and artifact. When a product manager can describe a feature, see a mockup, and get working code in the same conversation, the handoff-heavy workflow that defines most product development becomes optional. The design tools are a natural extension of Claude’s coding capabilities — once the model can write the code, generating the visual representation is a small step. For enterprise teams, the question is whether internal design review processes can adapt to a world where the first draft of a UI comes from a conversation, not a design sprint.

What to do: If your teams use Claude for development work, test the design capabilities on an internal tool or dashboard project. The value shows up fastest in internal apps where pixel-perfect design matters less than functional iteration speed.

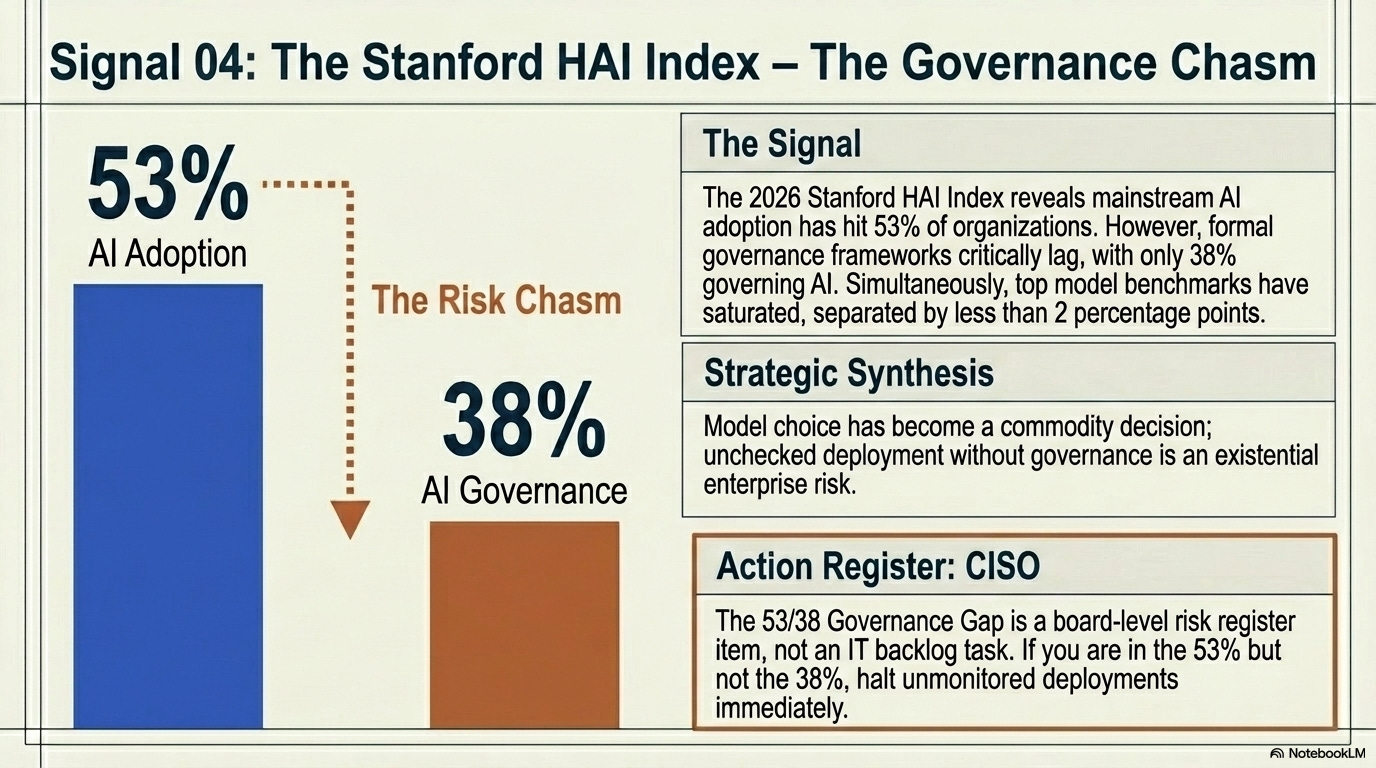

4. Stanford HAI releases 2026 AI Index — adoption accelerates, governance lags

What happened: Stanford’s Human-Centered AI Institute published its annual AI Index Report, documenting that 53% of organizations globally now use AI in at least one business function, up from 42% the prior year. The report found that AI governance adoption continues to trail deployment: only 38% of organizations with active AI deployments have formal governance frameworks. Model performance on standard benchmarks has saturated, with top models separated by less than 2 percentage points on most tasks.

Why it matters: The 53% adoption number confirms what the vendor earnings calls have been suggesting: AI is no longer early-adopter territory. But that 53/38 gap — 53% deploying, 38% governing — is the number that should keep CISOs up at night. Stanford just gave that claim a Tier 0 academic source: model choice is the least consequential decision in enterprise AI strategy. Benchmarks are saturated and gamed. That finding reinforces the argument I’ve been making since the Benchmarks Guide in February.

What to do: Download the full report and share the governance gap data with your CISO and legal team. If your organization is in the 53% deploying but not in the 38% governing, that gap is a risk register item, not a future initiative.

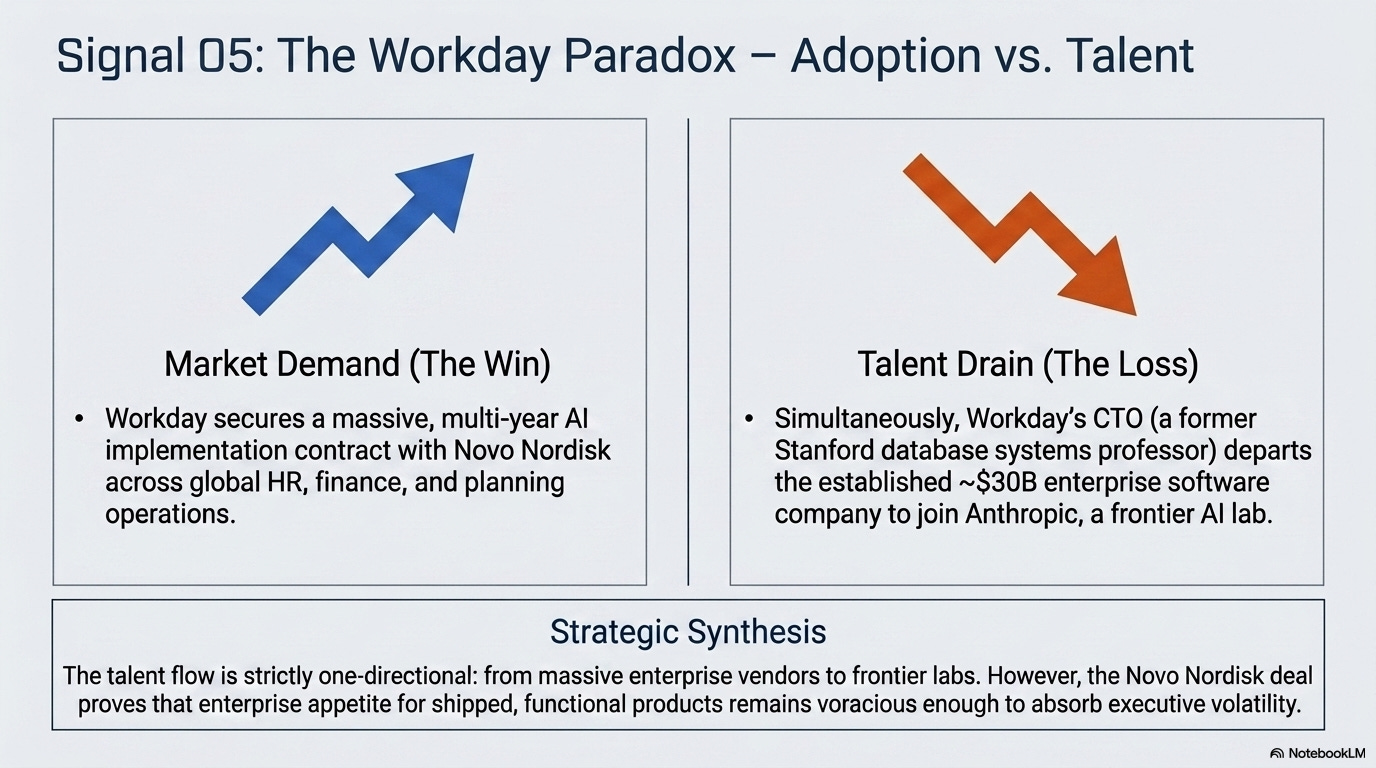

5. Novo Nordisk signs multi-year enterprise-wide Workday AI partnership

What happened: Novo Nordisk, one of the largest pharmaceutical companies by market cap, signed a multi-year enterprise-wide partnership with Workday to deploy AI-powered HR, finance, and planning capabilities across its global operations. The deal covers Workday’s full platform including Illuminate AI features, workforce planning, and financial management. Novo Nordisk will use Workday as its primary enterprise platform for AI-driven decision support across people and financial operations.

Why it matters: Pharma companies of Novo Nordisk’s scale don’t sign multi-year enterprise-wide AI platform deals casually. Workday’s AI capabilities have crossed the threshold from “interesting feature” to “enterprise bet” for at least one major buyer. The timing matters too: Workday just lost its CTO to Anthropic (see Signal 8), and landing a deal of this scope immediately afterward suggests the product roadmap is strong enough to survive executive departures. For enterprise architects evaluating Workday, the Novo Nordisk commitment is a meaningful reference point for AI readiness across HR and finance workflows.

What to do: If you’re evaluating Workday for AI-powered HR or finance, ask your Workday account team for any pharma reference customer who’s deployed Illuminate in a production environment. Don’t wait for Novo Nordisk specifically — any pharma company’s data governance requirements will stress-test Workday’s AI capabilities in ways that matter for any regulated industry.

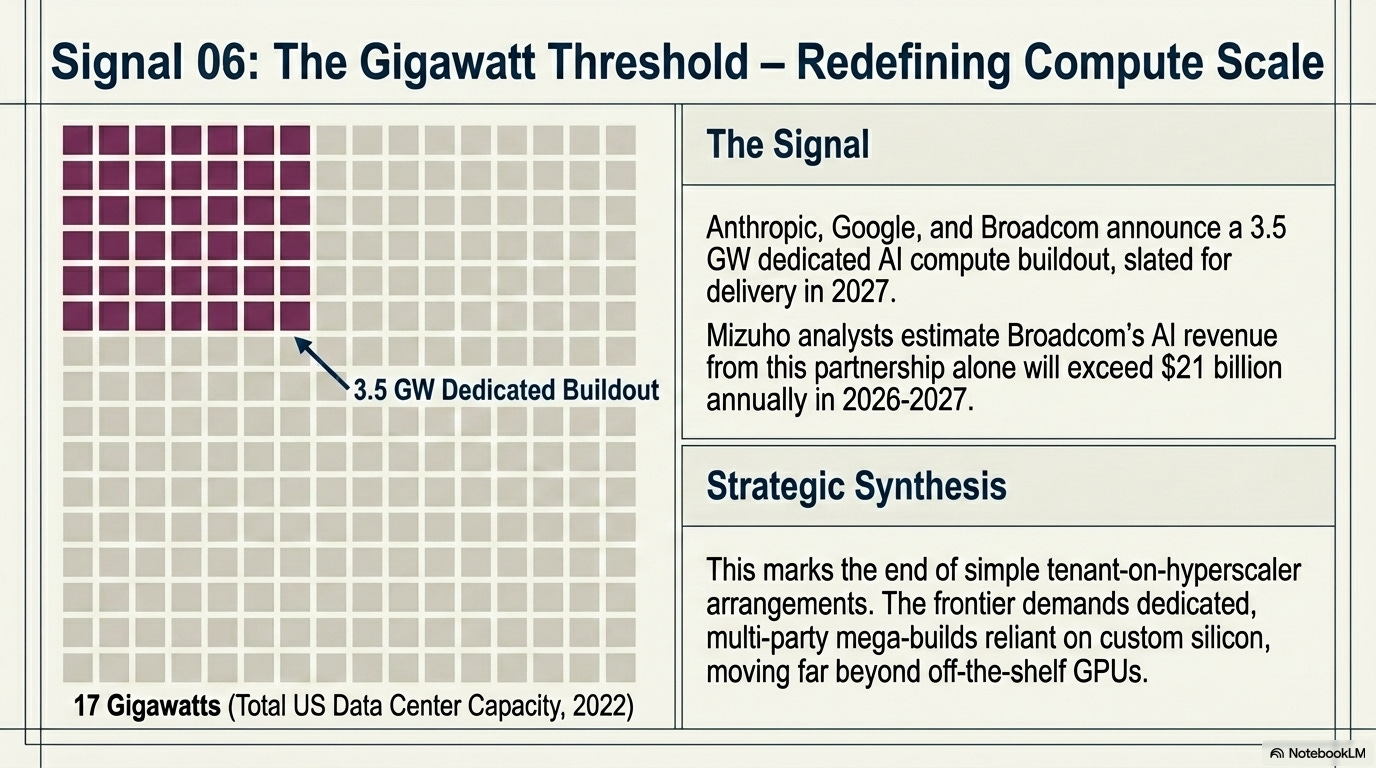

6. Anthropic, Google, and Broadcom announce 3.5 gigawatt AI compute partnership

What happened: Anthropic, Google, and Broadcom announced a partnership to build 3.5 gigawatts of dedicated AI compute infrastructure, with delivery starting in 2027. The SEC filing confirmed the capacity commitment but did not disclose a total dollar value. Broadcom will supply custom AI accelerators, Google will provide cloud infrastructure, and Anthropic will be the anchor tenant. Mizuho analysts estimate Broadcom’s AI revenue from this partnership could exceed $21 billion annually in 2026-2027.

Why it matters: 3.5 gigawatts is an extraordinary amount of compute capacity — for context, the entire US data center industry consumed roughly 17 gigawatts in 2022. This is one of the largest AI compute capacity commitments announced to date, and it represents a new model for AI infrastructure: a dedicated, multi-party buildout rather than a tenant-on-hyperscaler arrangement. Anthropic isn’t cloud-dependent anymore — Broadcom’s involvement proves it. Custom silicon, not off-the-shelf GPUs, is the path forward for frontier AI training at this scale. What this signals for enterprise leaders: infrastructure is no longer the commodity it was in the cloud era. Watch how pricing resets once this capacity comes online. Inference costs should decline.

What to do: Track the delivery timeline (2027) against your own AI infrastructure planning. If 3.5 gigawatts of new capacity comes online in 2027, inference pricing should decline. Factor potential price decreases into multi-year AI platform contracts you’re negotiating now — don’t lock in 2026 pricing for 2028 workloads.

7. Workday CTO Peter Bailis departs for Anthropic — talent migration accelerates

What happened: Peter Bailis, Workday’s CTO, departed in March 2026 to join Anthropic. Bailis, a Stanford database systems professor before joining Workday, led the company’s AI and machine learning strategy. The departure came from an approximately $30 billion enterprise software company (by current market capitalization) and is the latest in a clear pattern of senior technical leaders leaving established enterprise vendors for frontier AI labs.

Why it matters: The talent flow is one-directional: enterprise software to frontier labs. Bailis is the most prominent example this quarter, but he’s not alone. A CTO leaving a ~$30 billion enterprise software company for an AI lab tells you where the most ambitious technical leaders believe the highest-impact work is happening right now. For Workday specifically, losing the architect of their AI strategy creates a roadmap execution risk that customers should monitor. The Novo Nordisk deal (Signal 6) suggests the product pipeline is strong enough to absorb the departure, but CTO transitions at enterprise software companies have historically caused 12-18 months of strategic drift.

What to do: If you’re a Workday customer, ask your account team who is leading the AI roadmap now and whether the Illuminate product timeline has changed. If you’re evaluating Workday, weight the Novo Nordisk reference (Signal 6) more heavily than the CTO departure — shipped product matters more than org chart changes.

What signal did I miss? If you’re tracking enterprise AI moves in healthcare delivery, defense contracting, or energy infrastructure that should have made the cut, hit reply.

Past editions:

References:

Great post, Karthik. Your posts are a staple for me to stay current on the AI landscape; I always appreciate the perspective.

I’ve been reflecting on ServiceNow’s move to these "AI-native" tiers (Foundation/Advanced/Prime). While collapsing the add-on fees simplifies the bill, I’m curious if you’re seeing a significant jump in the base license costs for customers moving to these new tiers?

The part that really has me thinking, though, is the shift in the "automation lifecycle." In the "good old" workflow model, we followed a build-once/run-forever approach. With this new AI-native architecture, do you think we’re moving toward a model where the logic is effectively being "designed" every single time the process runs via an AI agent? Or is there a layer of optimization happening where a flow is "designed" once by AI and then cached/re-used?

If it's the former, aren't customers essentially paying a "design cost" (via usage-based Assists/tokens) for every execution, rather than amortizing a one-time build cost? It feels like high-volume, simple automation that we already "solved" with standard, deterministic flows might be getting pulled into a recurring consumption bucket.

I'd love to get your take; Is this a genuine step forward in flexibility, or are we seeing a rebranding of standard automation into "Generative Orchestration" to justify the new metering?